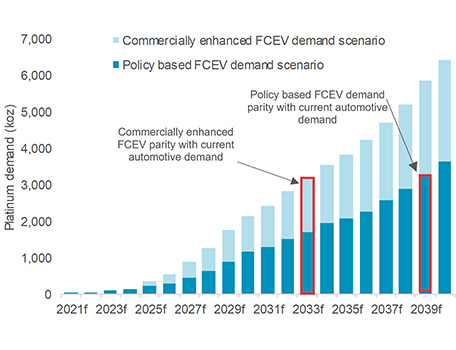

According to recent World Platinum Investment Council (WPIC) research*, it is just a matter of time until demand for platinum from fuel cell electric vehicles (FCEVs) equals the current level of platinum automotive demand, which is forecast to be over 3,000 koz this year.

FCEV platinum demand could exceed 3,000 koz as early as 2033 under WPIC’s ‘commercially-enhanced’ scenario, should effective government policies and initiatives spur on the growth of the FCEV market, with production and infrastructure critical mass resulting in economies of scale sufficient to promote widespread FCEV adoption on the grounds of costs and practicable usability. Under a more conservative policy-only based scenario, platinum FCEV demand would equal current automotive demand a little later, by 2039.

China – which has just seen the launch of its first mass-produced passenger FCEV, the Changan Shenlan SL03 – is well positioned to be one of the leading forces in the global FCEV market, especially in the mass transport and heavy-duty sectors. This is perhaps not surprising, given that, in 2019, China was home to approximately seven million heavy-duty trucks – or one third of the world’s 20 million heavy-duty trucks. Based on Bloomberg NEF predictions, by 2040, 50 per cent of the world’s heavy-duty trucks will be powered by clean energy.

Forefront of market

The International Energy Agency Advanced Fuel Cells Technology Collaboration Programme’s statistics show that 5,648 FCEV buses were in deployment globally as at the end of 2020; China is at the forefront of this market, with a fleet of 5,290, giving it an almost 94 per cent share.

The further expansion of the new energy vehicle (NEV) industry under China’s 2060 carbon neutral directive is also highly supportive of FCEV growth. According to China Association of Automobile Manufacturers (CAAM) statistics, 8,922 FCEVs were registered in 2021. Recent plans (NEV Industry Development Plan and NEV Technology Roadmap 2.0) will help to stimulate the market for FCEVs further. By 2035, the market share of NEVs in China is expected to exceed 50 per cent, with the number of FCEVs reaching around one million.

Broad-based commercial adoption of FCEVs could see additional platinum demand reach current automotive levels by 2033. Source: WPIC research

What is more, China’s plans to boost green hydrogen production are also supportive of FCEV penetration. Green hydrogen production capacity additions in China comprise 36 per cent of all planned projects globally. These additions support the roll-out of infrastructure such as hydrogen refuelling stations (HRS) that are needed to make FCEVs a viable consumer option.

China has taken an ambitious stance on HRS growth when compared to other countries, targeting 1,000 HRS by 2030 - an objective that is likely to be met well in advance of that date. In comparison, the next most ambitious targets are South Korea, at 310 HRS by 2022, and Germany, aiming for 400 HRS by 2023.

At a local level, more than 20 regions have so far issued phased plans for the promotion of FCEV deployment. Shanghai, for example, has recently proposed a 2023 target of ‘100 hydrogen refuelling stations, 100 billion yuan of industry output, and 10,000 FCEVs deployed’.

*WPIC – Platinum Essentials March 2022 ‘Fuel cell electric vehicles are forecast to drive material long-term growth for platinum’