According to the International Energy Agency (IEA)* electrolyser manufacturing capacity grew to reach nearly 11 gigawatts per year last year.

What is more, based on the current pipeline of projects under development and their expected operational dates, the IEA believes that global electrolysis installed capacity could reach almost 3 GW by the end of 2023, a more than four-fold increase in total capacity compared to 2022. Platinum-based proton exchange membrane (PEM) electrolysis accounts for around one third of this.

Further, if all the projects currently in the pipeline are realised, global electrolysis installed capacity could reach 170-365 gigawatts by 2030. Assuming a 30 per cent share, the PEM share of this market equates to between 50 and 110 gigawatts.

The electrolysis of water – when an electric current is used to separate water into its component elements of hydrogen and oxygen – is a well-established way of producing hydrogen. If the electric current is derived from a renewable source the hydrogen made is ‘green’. PEM electrolysers and alkaline electrolysers are the two leading electrolysis technologies commercially available.

PEM electrolysers, which contain a platinum catalyst, were first developed during the 1950s for the space programme; today, they have moved from the niche to the mainstream as the case for green hydrogen has strengthened, driven by: the need to find solutions to combat climate change; the improving business case for green hydrogen, based on growing renewable generation capacity and falling renewable electricity costs; and innovation in PEM technology.

Significant growth

The growth of green hydrogen in the world’s energy system is significant because of its long-term energy storage capabilities which could help to decarbonise transport, heating, and industrial processes. More than 30 countries have hydrogen strategies in place which focus on the deployment of green hydrogen to achieve net zero goals.

In the US, the government released its National Clean Hydrogen Strategy earlier this year, with the stated ambition of enabling multi-giga-watt scale electrolyser manufacturing capacity.

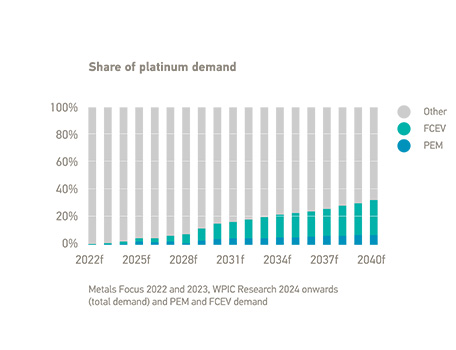

Hydrogen-related platinum is expected to grow substantially in the medium-term, becoming a meaningful component of global platinum demand by 2030, and potentially the largest demand segment for platinum by 2040

In parallel, the US’s Infrastructure Investment and Jobs Act (IIJA), enacted on 15 November, 2021, has a variety of initiatives to stimulate new markets for clean hydrogen, including US$1 billion of funding for a clean hydrogen electrolysis programme, aimed at improving the efficiency and cost-effectiveness of electrolysis technologies by supporting the entire innovation chain—from research, development, and demonstration to commercialisation and deployment to enable US$2/kg clean hydrogen from electrolysis by 2026. The IIJA also provides US$8 billion of funding for the provision of Regional Clean Hydrogen Hubs.

Recent developments highlight how both manufacturing capacity and deployment are ramping up. In the first quarter of 2023 Plug Power Inc (Plug) announced it had manufactured 122 megawatts of its one-megawatt PEM electrolyser stacks at its 2.5-gigawatt factory in the US, achieving an all-time high for the industry. It is on track to increase output to 100 megawatts per month there during the remainder of the year. In May, Plug announced a joint venture in South Korea with SK Group to build an electrolyser and fuel cell giga factory.

The UK’s Johnson Matthey is working with PEM electrolyser developer Hystar, to enable further scale up and automation for Hystar’s planned multi gigawatt production line, which is expected to be operational by 2025. Meanwhile, Nel has announced plans to build a new automated gigawatt PEM and alkaline electrolyser manufacturing facility in Michigan, US. When fully developed, the facility be among the largest electrolyser manufacturing plants in the world.

While hydrogen-related platinum demand is currently relatively small, it is expected to grow substantially in the medium-term, becoming a meaningful component of global platinum demand by 2030, and potentially the largest demand segment for platinum by 2040.

*IEA: Tracking Clean Energy Progress, 12 July 2023