A platinum deficit of over one million ounces is now forecast for 2023. Strong automotive demand growth is a key factor behind the widening deficit, in addition to industrial demand growth to record levels, and flat supply. Platinum automotive demand is expected to reach 3,283 koz in 2023, up 13 per cent on 2022, the highest level since 2017.

While automotive demand for platinum continues to be driven primarily by platinum-for-palladium substitution, which is forecast to reach 615 koz in 2023, and higher loadings, it has received a boost from higher-than-expected growth in vehicle production during the second quarter of 2023. This is because the impact of the semiconductor shortage and other supply-chain challenges experienced by the automotive industry as a result of the pandemic and, more latterly, the Russian invasion of Ukraine, have eased considerably.

During the quarter, light-duty vehicle (LDV) production saw a healthy increase of 14 per cent year-on-year, while heavy-duty vehicle (HDV) production improved by 18 per cent. Despite challenging macroeconomic conditions and cost of living concerns, demand for new vehicles exceeded supply, which supported higher production rates.

Regional overview

In North America, vehicle production improved by 15 per cent year-on-year in quarter two. Platinum demand in the region improved due to a combination of a greater share of hybrid vehicles and higher platinum loadings – both the consequence of increased substitution of platinum for palladium and higher overall loadings to meet tighter emissions limits.

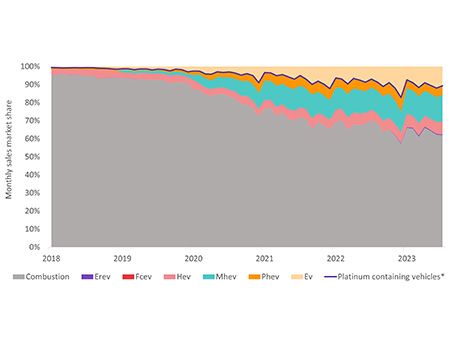

In Europe, platinum automotive demand increased by 11 per cent on the back of strengthening LDV production which also increased 11 per cent year-on-year. Even though Europe is one of the leading geographies for battery electric vehicle adoption, around ninety percent of the vehicles sold still contain platinum in their aftertreatment systems.

Around 90% of the vehicles sold in Europe still contain platinum in their aftertreatment systems. Source: Bloomberg, WPIC Research

Automotive demand for platinum in China during the quarter surged by 60 per cent. This was largely attributable to the implementation of China IV for non-road vehicles, as well as the HDV segment, where output recovered by 64 per cent, while LDV production grew by 17 per cent. In addition, the full implementation of China VIb, which came into force on 1 July 2023, has had an impact. These emissions regulations have seen China ban the production, import and sales of trucks and buses that fail to meet the new standard, despite some attempts to delay the implementation to 2024. A fourth factor that strengthened Chinese platinum demand was the increased substitution of platinum for palladium in exhaust treatment systems.

Japan’s LDV production of petrol and diesel cars increased by 20 per cent compared to the same quarter in 2022, which was heavily impacted by semiconductor shortages. Meanwhile HDV production rose by a more moderate six per cent. These higher production rates supported a 29 per cent year-on-year increase in platinum automotive demand.

Elsewhere, production also improved by 11 per cent year-on-year, resulting in a further lift in platinum demand.