Derived from the same ore, the Platinum Group Metals (PGMs) – platinum, palladium, rhodium, ruthenium, iridium and osmium – are a family of six individual elements that have similar chemical and physical characteristics. They have complementary properties that can be leveraged and combined to meet specific requirements, depending on the application.

Electrocatalysts containing the PGMs platinum and iridium are used in proton exchange membrane (PEM) electrolysis to make hydrogen. When produced using renewable electricity, this is termed ‘green hydrogen’, a carbon-free energy carrier that is increasingly viewed as essential to the energy transition. During electrolysis, water is split into its constituent parts, oxygen and hydrogen, using electricity.

According to the Hydrogen Council, electrolyser capacity grew by 30 per cent in 2022 to 170 megawatts, bringing total capacity to 700 megawatts. PEM electrolysis represents around 30 per cent of this market. Hydrogen momentum remains strong, and looking ahead to 2050, the International Energy Agency (IEA) estimates total electrolyser capacity will reach 4,000 gigawatts, implying 1,550 gigawatts of cumulative installed PEM electrolyser capacity if the current market share of PEM electrolysis is maintained.

Iridium is some 20 times scarcer than platinum. Global iridium supply is about 250 koz per year – roughly in balance with current demand, which includes its use in spark plugs, crucibles and acetic acid production.

For every gigawatt of PEM electrolyser capacity, around 400 kg of iridium is currently required. Should capacity growth continue at the pace expected, iridium demand from electrolysis alone could equal current annual supply by 2030, implying that a shortfall in iridium supply will occur. There have been some concerns that a shortage of iridium could potentially impede the growth of PEM electrolyser capacity and, consequently, associated platinum demand, given that PEM electrolysis is a growing new end-use segment for platinum.

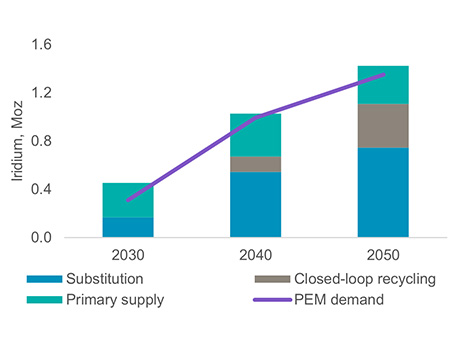

Sufficient supply

However, research from the World Platinum Investment Council (WPIC) shows that through a combination of: substitution of alternative PGMs for iridium in other applications; thrifting; and recycling, iridium supply will be sufficient to meet PEM electrolyser demand as it grows – even to the 2050 level envisaged by the IEA. This growth, WPIC estimates, could see incremental platinum demand from PEM electrolysis reach 500 koz per annum by the early 2030s.

Cumulative iridium demand from PEM electrolysers is met in the next three decades, with 1,550 gigawatts of projected capacity by 2050. Source: WPIC forecasts

Economic factors drive substitution decisions, and the iridium price has outperformed other PGMs over the past three years. The automotive (i.e. spark plugs) and electronic (i.e. crucibles) sectors are reportedly already substituting some iridium. Cumulatively, WPIC estimates 20 per cent of existing iridium demand will be substituted by 2030 and 30 per cent by 2040, freeing up annual iridium supply of between 45 koz and 67 koz over the next decade.

Thrifting – reducing the loading of iridium needed per gigawatt in a PEM electrolyser – is already underway and 100 kg per gigawatt catalysts are close to coming to market. Johnson Matthey believes 80 kg per gigawatt loadings are feasible by 2030 and Heraeus cites that the next generation of technologies is targeting further reduction of iridium loadings to 30 kg per gigawatt by 2050.

The emphasis on increasing circularity in manufacturing processes and supply chains, with particular regard to the ‘end of life’ product stage by ensuring re-use and recycling of materials wherever possible, is growing. For example, the US’s clean hydrogen roadmap targets a 99 per cent recycling rate of PGMs within electrolysers by the 2030s.