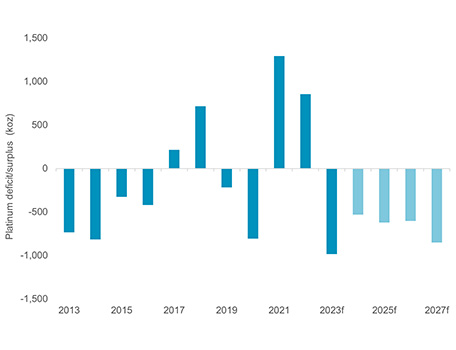

Platinum is expected to transition into a supply deficit from 2023, with consecutive supply/demand shortfalls being sustained through to 2027 when it will reach a deficit of 851 koz. Multi-year platinum shortages, accentuated by ongoing substitution of platinum for palladium in automotive end uses, will drawdown above ground platinum stocks and tighten markets at a time of rapid acceleration in the growth of the hydrogen economy.

While hydrogen-related platinum demand from proton exchange membrane (PEM) technology is currently relatively small, it is expected to grow substantially in the medium term, becoming a meaningful component of global platinum demand by 2030, and potentially the largest demand segment for platinum by 2040.

Platinum and palladium are co-products in polymetallic ores, typically found in association with the other platinum group metals (PGMs), including rhodium. Platinum and palladium, along with rhodium, are key materials used in autocatalysts for reducing harmful vehicle emissions. Although there are some physiochemical differences, as part of the PGM group they are similar enough to be interchangeable, to a point, in many applications, and specifically in autocatalysts.

Commodity prices are impacted by supply demand/imbalances. In the event of oversupply, the price of a commodity would normally be expected to fall until uneconomic supply is curtailed, or the price falls to a level that attracts new demand into the market. Conversely, in the event of a market being in undersupply, the price of a commodity is normally expected to increase until new supply is attracted to the market, or demand is priced out of the market. The polymetallic nature of PGM bearing orebodies means that there are multiple price inputs establishing the economics of production. Thus, mine supply is unlikely to react to the changing fortunes of any one specific commodity. Primary mine supply is therefore highly (but not totally) price inelastic.

However, the ability to substitute platinum for palladium and vice versa in certain applications helps, to an extent, to balance the market over time, with the automotive sector historically switching between PGMs when market imbalances arise.

Platinum is forecast to move into market deficit from 2023. Source: Metals Focus 2013-2023f, WPIC Research 2024 onwards

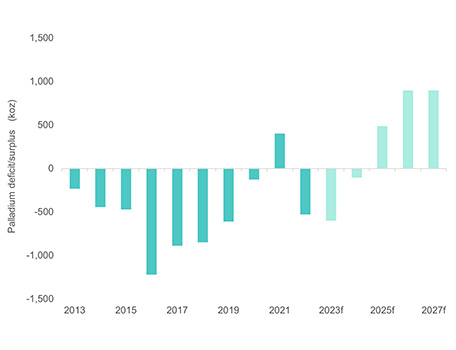

Palladium is forecast to move into market surplus from 2025. Source: Metals Focus 2013-2022, WPIC Research 2023 onwards

Reverse substitution

Since 2017, when the palladium price began to exceed the platinum price, price differentials and – more latterly – security of supply concerns have driven platinum-for-palladium substitution in emissions control systems. By the end of 2023, cumulative platinum-for-palladium substitution over the last five years will have reached an estimated 1,300 koz.

As platinum heads into a series of sustained market deficits from this year and palladium moves towards a series of market surpluses from 2025, WPIC anticipates an eventual closure of the platinum/palladium pricing differential. Consequently, it expects the trend of platinum-for-palladium substitution to slow, and eventually cease, with palladium-for-platinum ‘reverse’ substitution occurring from 2025.

The expected palladium-for-platinum reverse substitution will only be in small volumes initially as the substitution process is a lengthy one given it is almost always only conducted on new models and is then locked in for the lifetime of those models, typically seven years. It will therefore take a long time to even unwind the platinum for palladium substitution that is currently occurring and that is projected to peak in 2025. Even so, by 2027 WPIC forecasts palladium for platinum substitution to reach 366 koz, and to continue to grow thereafter.

Positively, this will liberate platinum supply to become available for the rapid growth in the hydrogen economy expected in the mid-to-late 2020s, alleviating concerns that platinum could prove to be a bottleneck in the development of the PEM technology that is key to the energy transition.