‘Inelastic’ is a term used by economists to describe a situation where a change in price has a relatively small impact on the quantity demanded of a good or service. In other words, consumers will continue to purchase roughly the same amount even if the price increases or decreases.

In contrast, an elastic relationship means that changes in price will result in a significant increase or decrease in the supply or demand of a good or service.

Platinum prices have recently reached a ten-year high, exceeding $1,420/oz as of 26 June. This follows a prolonged period when platinum’s price was stuck at a range which varied from around $900-$1,100/oz.

Yet, because the relationship between the price of platinum and its supply or demand is largely price inelastic, the platinum price rally is unlikely to dampen demand or stimulate miners to produce additional metal, meaning that, in the platinum market, supply will continue to lag demand, resulting in a structural deficit.

To put this in context, the platinum market is expected to record its third successive shortfall this year, at 966 koz. This follows deficits of 992 koz and 896 koz in 2024 and 2023, respectively. Moreover, looking at the WPIC two to five-year forecast through to 2029, deficits are forecast to occur every year.

Robust demand

Consecutive supply deficits are expected to see above ground stocks run out by 2029. Meanwhile, platinum supply remains challenged, both in terms of primary mining and secondary recycling supply. At the same time, the demand outlook is robust. Demand for hybrid vehicles and slower-than-expected battery electric vehicle adoption is supportive of platinum automotive demand, while strong demand growth in both investment and jewellery is being experienced in China.

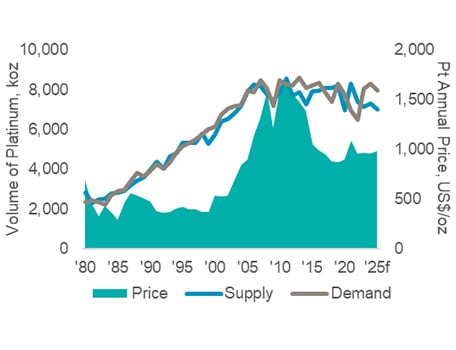

Chart 1: Platinum supply and demand have historically shown little short-term sensitivity to price movements. Source: Johnson Matthey 1980-2012, SFA (Oxford) 2013-2018, Metals Focus 2019-2025f

Chart 2. Despite sharp price increases, the PGM basket has failed to drive any meaningful gains in overall supply. Source: Johnson Matthey 1997-2012, SFA (Oxford) 2013-2018, Metals Focus 2019-2025f

Data supports the view that both platinum supply and platinum demand are largely price inelastic in the medium term. Chart 1 illustrates that historical movements in the platinum price did not trigger an immediate change in supply or demand, with responses often lagging by several years.

On the supply side, platinum’s inelasticity is structural. As Chart 2 demonstrates, even sharp price signals take years to translate into new supply – most mines require eight to nine years to reach full production capacity, and investment decisions must take into account not only platinum’s price potential, but also that of the overall platinum group metals basket plus base-metal by-products.

Demand is also unlikely to fall in the short-term, despite the price rally making platinum more expensive for industrial end users. Across the automotive, jewellery and industrial sectors, platinum consumption has historically shown limited volatility in relation to short-term price movements. Between 2003 and 2008, for instance, automotive demand rose by over 25% even as prices climbed from around $600 to $2,000/oz, only falling after the global financial crisis precipitated a broader widespread commodity downturn.

Industrial demand has shown some delayed inverse relationship with price, but volumes tend to adjust over multiple years. Jewellery is structurally more elastic, yet platinum’s relatively more attractive affordability versus gold is now emerging as a counterforce. The gold-to-platinum price ratio reached 3.5x in May 2025, its highest level since 2015, prompting some Chinese fabricators to switch to platinum.