18 April 2024: Latest Russia sanctions unlikely to impact near-term PGM markets, but there may be longer term benefits: Latest Russia sanctions unlikely to impact near-term PGM markets, but there may be longer term benefits: Russia accounted for 28% of primary 2E PGM supply in 2023 as a by-product of base metal mining from polymetallic ore bodies. We see a limited impact from the latest round of base metal sanctions; like after the April 2022 PGM sanctions by the London Platinum and Palladium Market, metal will continue flowing. However, the latest sanctions probably eliminate any expectations of supply growth from Russia, which given its importance to class 1 nickel markets may slow BEV growth rates and support higher for longer ICE PGM demand.

Platinum Perspectives

WPIC® research is free of charge. It can be consumed by asset managers under MiFID II

28 March 2024: Revised US emission timelines support higher for longer PGM demand : Revised US emission timelines support higher for longer PGM demand: The United States has finalised its vehicle emission reduction targets for 2032. These targets are unchanged from those proposed in April 2023, however, the interim thresholds leading up to the 2032 targets have been made more lenient. This follows a growing global trend of concessions on emission reduction timelines which cumulatively extends the role of ICE vehicles mainly through hybrid technology, which supports higher for longer ICE demand for PGMs.

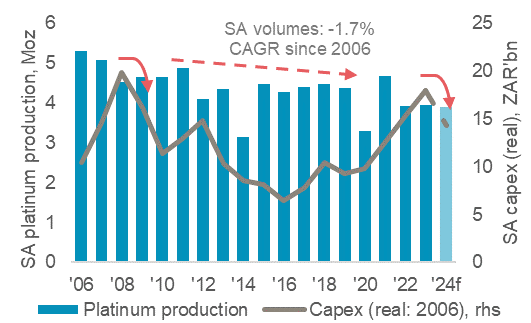

27 March 2024: Platinum’s supply risks cannot be overlooked as PGM prices remain weak and miners reduce capex: Platinum’s supply risks cannot be overlooked as PGM prices remain weak and miners reduce capex: South African PGM miners have all announced cost focussed restructuring in response to a lower PGM basket price during 2023. While restructuring announcements are not expected to materially impact near-term production, supply risks cannot be overlooked. Previous instances of declining capex have contributed to a slow decline in output. Should future supply match past reduced-capex trends, a supply risk of -250 koz per annum by 2028 could materialise and further deepen projected market deficits.

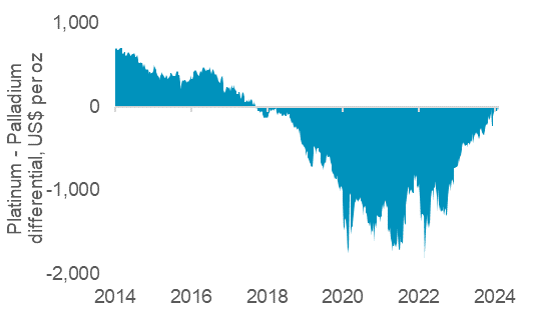

27 February 2024: With palladium oversold and platinum’s attractive fundamentals, both metals have upside : With palladium oversold and platinum having attractive fundamentals, both metals have price upside: Palladium’s recent price fall to platinum sees the sister metals now priced at near parity for the first time since 2018. This palladium price fall has been long-expected, due to forecasts of palladium moving into surplus from 2025. However, a build in net managed money short positions leaves it vulnerable to short squeezes, and a potential delay to recycling growth could keep the market in deficit for longer. In contrast, platinum’s fundamentals are much more attractive, with the current market deficit expected to continue until at least 2028. This should be reflected in the price after excess automaker inventory management has run its course.

_129341.png?v1)

24 January 2024: Platinum for palladium substitution is embedded into automotive demand and unlikely to reverse swiftly : Platinum for palladium substitution is embedded into automotive demand and unlikely to reverse swiftly: Platinum for palladium autocatalyst substitution is expected to reach 700 koz in 2024f, up from 620 koz in 2023f. Our analysis shows that there are no economic incentives and a number of risks to reversing this process. Furthermore, the process of reverse substitution will be slow, even if it does occur. Thus, existing substitution is largely embedded in annual automotive demand for the medium term.

_440099.png)

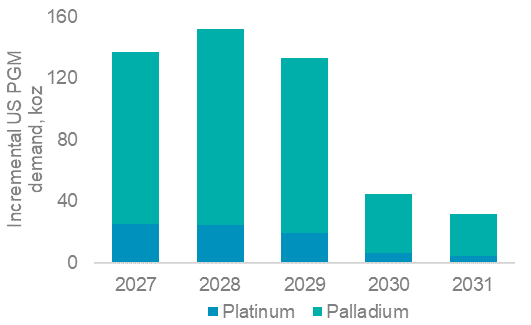

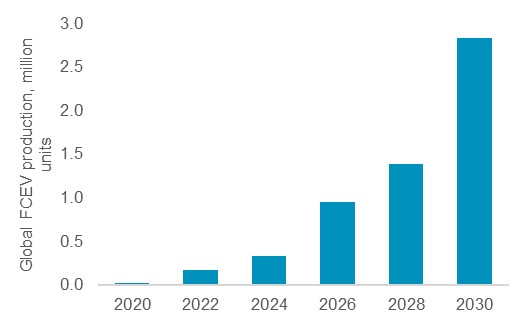

19 December 2023: South Korea’s H2 plans support future platinum demand : South Korea’s strategy to decarbonise its highly industrialised economy relies heavily on using green hydrogen, which will result in it becoming a significant platinum demand hub. South Korean hydrogen linked demand for platinum is expected to reach 300 koz pa by 2030, from its use in electrolysers to produce green hydrogen and its inclusion in Fuel Cell Electric Vehicles.

_249405.png)

7 December 2023: Sustained recycling challenges could deepen platinum supply-demand deficits: Sustained recycling challenges could deepen platinum supply-demand deficits: An examination of factors influencing constrained recycled autocatalyst supply suggests that challenges which were previously deemed short-term may be multi-year considerations. Lower automotive scrap was initially attributed to suppressed new vehicle production because of disruptions from COVID and the semiconductor shortage. However, with light vehicle recovering in 2023, automotive recycling has continued to shrink. Should automotive recycling rates not recover and stabilise at the 2024 forecast levels, platinum supply could be reduced by an aggregate 900 koz between 2025f to 2027f.

26 October 2023: Hydrogen Tech Expo: Evidence of growing momentum, with platinum set for key role as a transition metal : The hydrogen economy is building momentum, with electrolysis and fuel cell markets expected to account for up to 20% of total platinum demand by 2030. WPIC attended the European Hydrogen Tech Expo. Participants highlighted key developments in decarbonisation policy over the past twelve months. Better policy certainty is expected to accelerate investment decisions. Green H2 electrolysis is expected to increase 30-fold to ~500 GW by 2035 while levelised costs will reach parity with grey H2 in the next decade. This report offers a snapshot of developments in fuel cell use in automotive transport from the Expo.

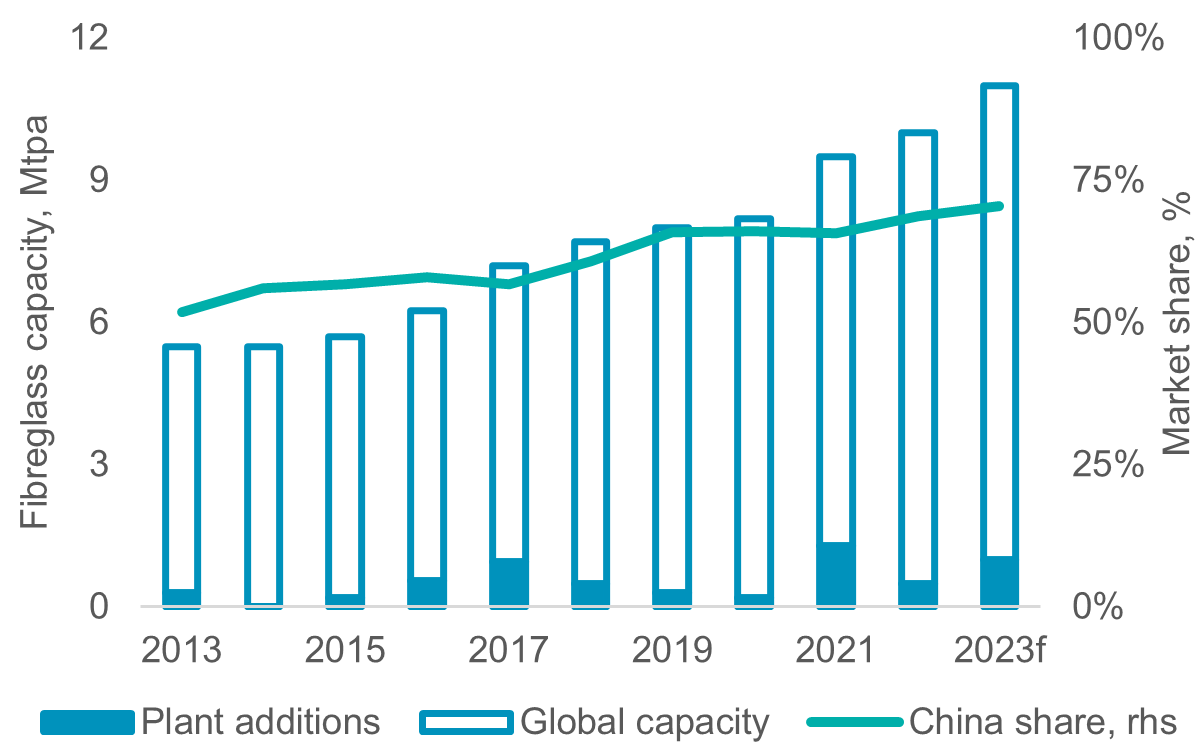

27 September 2023: China’s demand for glass fibre continues to grow, supporting ongoing platinum industrial demand growth: Strong growth in global glass and glass fibre demand has been a major factor behind platinum industrial demand growth of 5.4% CAGR over the last decade, double that of global GDP growth. Despite glass capacity growth being cyclical, our analysis suggests that ongoing growth in the renewable energy industry and automotive lightweighting will support sustained glass fibre demand growth and therefore industrial platinum demand growth.

14 September 2023: Punitive tariffs against Chinese automakers could slow European BEV adoption and boost platinum demand: A hurdle to mass-market BEV adoption is affordability. A successful bid by Brussels to apply anti-dumping tariffs onto Chinese electric vehicles sold within the bloc will increase costs and slow BEV adoption rates. Deferring BEV adoption will support Europe’s automotive platinum demand, potentially adding 200koz over the period 2025-7.