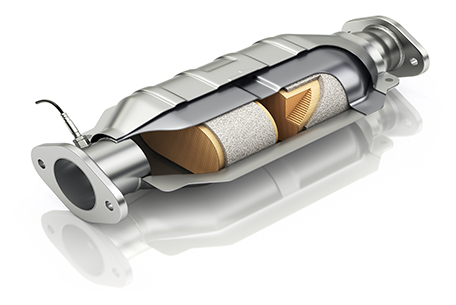

Patterns of use between platinum, palladium and rhodium in autocatalysts have varied over time, while emissions standards have grown ever more stringent. Usage is determined by multiple factors including the effectiveness, availability and price of each metal.

The catalytic efficiency of each metal is influenced by engine temperature, fuel type, fuel quality and durability of the autocatalyst’s washcoat. Today, platinum is predominantly used in autocatalysts in diesel vehicles, with palladium principally in those in gasoline vehicles. However, this usage is shifting, with substitution of palladium for platinum occurring due to sustained palladium deficits and the high price of palladium, now over US$1,300/oz higher than platinum.

PGM demand

Historically, tightening emissions legislation rather than changes in volumes of vehicle sales have driven PGM automotive demand growth. Between 1990 and 2019 annual car sales rose from c.54 m to c.92 m, while PGM use in autocatalysis rose from 2.2 moz per annum to 13.8 moz per annum.

Tightening emissions standards for oxides of nitrogen, including more stringent on-road rather than laboratory testing, continue to require more PGM per car, as does the use of low-carbon dioxide hybrid and mild-hybrid vehicles. This is because greater PGM loadings are required on these vehicles, which operate at cooler engine temperatures in their start-up phase.

The imperative for lower carbon dioxide emissions, to contribute to global climate change reduction goals, is reinforcing demand for diesel engine cars (including diesel hybrids), which have a 20 to 35 percent carbon dioxide benefit over gasoline engine cars. This, in addition to substitution, is a dominant driver for platinum demand growth.