Vowing to ‘build back better’, the new US president has placed climate change high up his administration’s agenda with plans to achieve 100 per cent clean energy and to commit to net zero by 2050. Underlining its intent, the US re-joined the Paris Climate Agreement, an international treaty on climate change with a goal to limit global temperature rise to below two degrees Celsius, on the president’s first day in office.

The president has promised a US$2 trillion accelerated investment over his first term aimed at building a modern, sustainable infrastructure to support the transition to a clean energy economy. This bodes well for zero emission hydrogen technologies which are likely to be an integral part of achieving the US’s climate change objectives.

A recent report, ‘Roadmap to a US Hydrogen Economy*’, forecasts that hydrogen from low-carbon sources could supply around 14 per cent of the country’s energy needs by 2050. According to the report, hydrogen is at a turning point in the US, with evidence of ‘sector coupling’ underway.

Sector coupling refers to the integration of energy-consuming sectors – buildings (heating and cooling), transport, and industry – with the power-producing sector. It leads to economies of scale as systemic benefits start to kick in: infrastructure costs are shared across applications and technological developments can be applied in multiple ways.

Projects that are boosting the US’s green hydrogen trajectory include the US$150 million Air Liquide biogas renewable liquid hydrogen plant in Nevada due in 2022, with a 30-ton daily generation capacity – enough to supply 42,000 fuel cell vehicles. In November last year, US-based Cummins, a global power leader, announced plans to grow its fuel cell and hydrogen production businesses. As part of the US Department of Energy’s H2@Scale initiative Cummins is developing a class 8 truck powered by hydrogen fuel cells.

Platinum the enabler

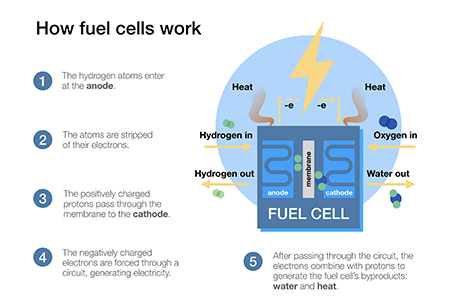

Platinum sits in the sweet spot for facilitating the hydrogen economy due to its use in not only generating green hydrogen, but also in fuel cells for fuel cell electric vehicles (FCEVs). FCEV growth in the US is currently being led by heavy-duty vehicle applications in ports and for road haulage. This builds on growth from fleet vehicles such as forklifts, with passenger cars a longer-term prospect – although there are already around 8,000 passenger FCEVs and 44 hydrogen refuelling stations in the state of California, which has taken a lead on decarbonisation.

As the hydrogen economy and the FCEV market grows in the US and elsewhere, it will create significant demand for platinum in the medium-term. In the EU and China alone it is estimated that green hydrogen production will require between 300 koz and 600 koz of platinum by 2030; the US’s decarbonisation goals and concomitant growth in green hydrogen projects will only add to these volumes. These developments increase the certainty of a hydrogen future, a factor which has driven significantly more investor interest in, and ownership of, platinum since 2019.

*Produced by a coalition of companies from the energy, transportation, fuel cell manufacturing and electric power industries with analytical support provided by McKinsey & Company