Volumes are a function of both the availability of spent autocatalysts and the extent to which participants in the recycling value chain are economically incentivised

Recycling forms a core component of platinum group metal (PGM) supply, for example accounting for an average of 24% of total platinum supply over the five years to 2024. PGMs retain their functional properties after recycling which means that recycled metal is interchangeable with mined metal in end-use applications, allowing PGMs to play an important role in the circular economy and sustainable design practices.

The recyclability of platinum is becoming increasingly key to overall platinum supply, as developed economic PGM mine reserves deplete. This year, platinum mine supply is forecast to decline 6% to 5,426 koz, some 701 koz (11%) below the five-year pre-COVID average and the lowest level for five years.

Automotive recycling supply comes from the recovery of PGMs – platinum, palladium and rhodium – contained within the autocatalysts in end-of-life vehicles. Automotive recycling makes up 75- 84% of total PGM recycling supply, depending upon the metal, with palladium the dominant metal when it comes to the economics of automotive recycling.

With the first autocatalysts fitted to cars in the 1970s, significant quantities of ‘in-use’ PGMs have accumulated and are theoretically able to support future supply requirements. Globally, legislation does promote recycling and the PGM industry has a mature recycling supply stream.

However, in practice, PGM automotive recycling volumes are a function of both the availability of spent autocatalysts and the extent to which participants in the recycling value chain – especially scrapyards – are economically incentivised to recycle autocatalysts.

Price elastic

WPIC research has identified that automotive PGM recycling supply is more price elastic than traditionally believed, meaning that at times when PGM prices are low, recycling supply is more likely to contract. This was the case in point for platinum between 2022 and 2024, when depressed platinum recycling supply was, at least in part, attributable to hoarding by scrapyards because it was less economically viable for them to trade spent autocatalysts during this period of low PGM prices.

Notably, scrapyards can hoard autocatalysts because they recognise multiple revenue streams from recycling vehicles with everything from steel, fabrics and used engine oil being recycled when a vehicle is scrapped.

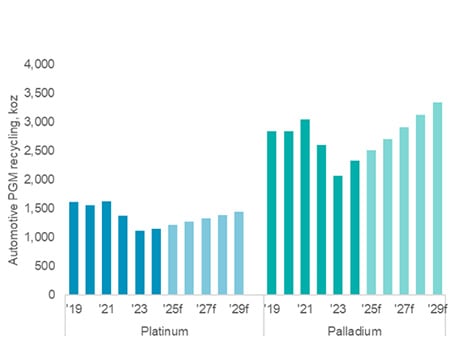

Recent PGM price increases have improved recycling economics and platinum and palladium automotive recycling supply is forecast to increase 6% and 8%, respectively, in 2025.

Looking out further, platinum automotive recycling supply is expected to continue to grow, with a 4.7% compound annual growth rate (CAGR) from 2024 to 2029. Palladium recycling is also expected to grow further, with a 7.5% CAGR over the same period. Both these forecasts are underpinned by the increasing availability of spent autocatalyst supply and the improved economic incentive to recycling given year-to-date PGM price increases.

However, since automotive PGM recycling supply is price elastic, growth in platinum recycling supply could be curtailed by the expected transition of palladium markets into surplus from 2027, given palladium’s dominance in recycling economics. This is because palladium market surpluses could mean that potentially lower palladium prices may once again disincentivise scrapyards from trading spent autocatalysts, encouraging hoarding.

Current price levels drive a modest increase in platinum and palladium recycling expectations before being capped by palladium moving into oversupply. Source: Metals Focus 2019 and 2024 (Pd) and 2025 (Pt), WPIC research thereafter