End of life autocatalysts are a key source of recycling supply, however, only at economically viable PGM prices

20 August 2025

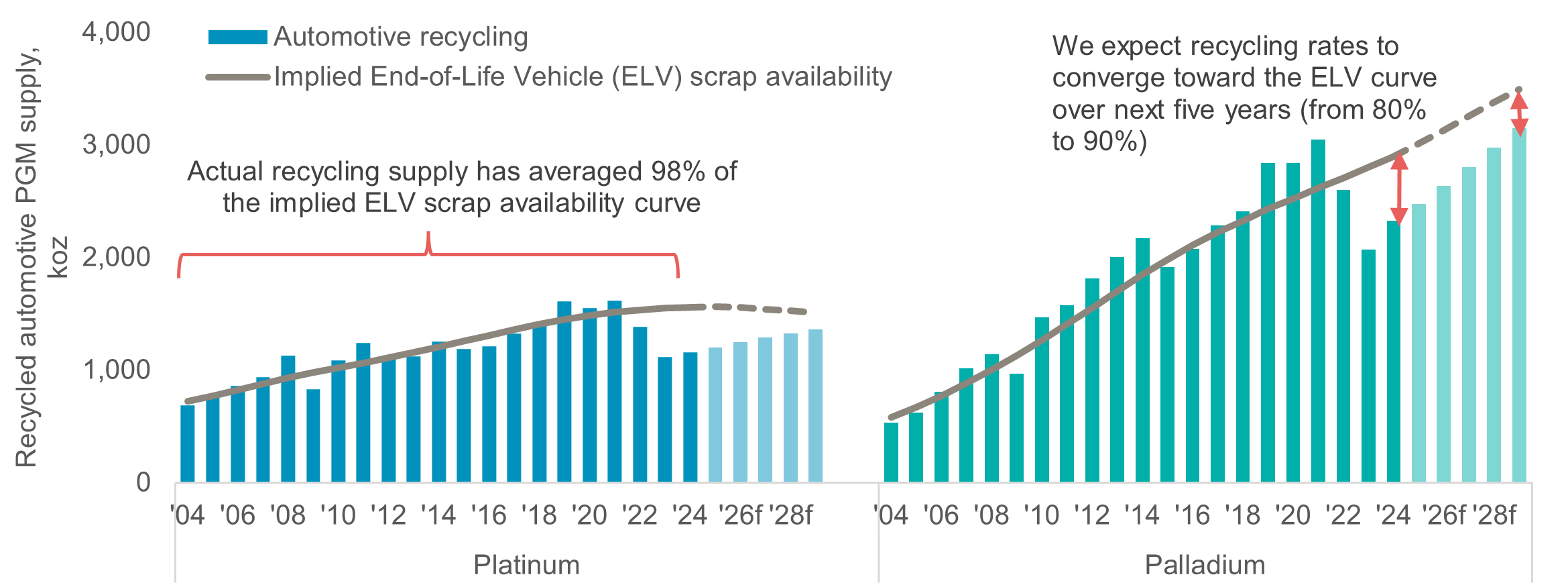

In this Platinum Essentials, we assess the value chain associated with recycling platinum group metals (PGMs) within the automotive industry. Recycled automotive PGM supply has recently been more price elastic than traditionally believed, explaining why recycling supply forecasts heavily undershot from 2022 to 2024. Higher PGM prices in 2025 are supportive of supply growth. However, platinum automotive recycling supply will not recover above peak levels reported in 2021 and we expect this to contribute to expected platinum market deficits to 2029f.

PGMs are, for the most part, infinitely recyclable, which supports their use in sustainable circular economies. With the first autocatalysts fitted to cars in the 1970s, significant quantities of “in-use” PGMs have accumulated and are theoretically able to support future supply requirements. Globally, legislation does promote recycling and the PGM industry has a mature recycling supply stream. However, in practice, we consider 1) the availability of spent autocatalysts and 2) the economic incentive to recycle autocatalysts to be the fundamentals that underpin PGM recycling volumes. Notably, the economic performance of recycling PGM supply may often be overlooked, in part because the value chain is opaque. Market participants may assume recycled PGM supply is completely price agnostic because refiners of scrap material generate stable margins through price cycles. This simplified assessment of recycling supply ignores the different gearing to PGM prices faced by scrapyards and aggregators that impact on recycled supply volumes. This impact should be considered together with mine supply risks. Our analysis highlights that recycling supply is price elastic. The decline in the PGM basket price from 2022 to 2024 materially reduced recycling supply leading to persistent downgrades in forecasts. Conversely, high PGM basket prices supported upgrades to automotive recycling forecasts from 2019 to 2021.

Consequently, within our five-year outlook to 2029f, we have downgraded our annual automotive recycling supply forecasts by 66 koz (-5%) for platinum and 226 koz (-7%) for palladium. However, we still expect automotive recycling supply to increase by 3.3% CAGR and 6.2% CAGR from 2024 to 2029f for platinum and palladium respectively. This is underpinned by the increasing availability of spent autocatalyst supply and the year-to-date rise in the basket price. However, since automotive PGM recycling supply is price elastic, growth in platinum recycling supply could be capped by the transition of palladium markets (dominant metal in recycling economics) into surplus from 2026f. Accordingly, we expect platinum automotive recycling supply to recover to only 90% of the available supply implied by end-of-life vehicle (ELV) scrappage curves (vs. 80% from 2022 to 2024 and 110% from 2019 to 2021).

Contacts:

Edward Sterck, Research, [email protected]

Wade Napier, Research, [email protected]

Brendan Clifford, Head of Institutional Distribution, [email protected]

WPIC does not provide investment advice.

Please see disclaimer for more information.