A hawkish US Fed is a headwind to platinum markets, but there could be signs of a turnaround from late 2026

24 June 2026

In updating our medium-term platinum market forecasts (link), we highlighted that platinum’s underlying fundamentals were structurally resilient but challenged by negative sentiment. The unambiguously hawkish tone of new US Federal Reserve Chair, Kevin Warsh, adds downward pressure on the precious metals complex. However, with a MoU between the United States and Iran signed and the Strait of Hormuz reopening, this could be the catalyst investors need to re-engage with precious metals around the end of 2026.

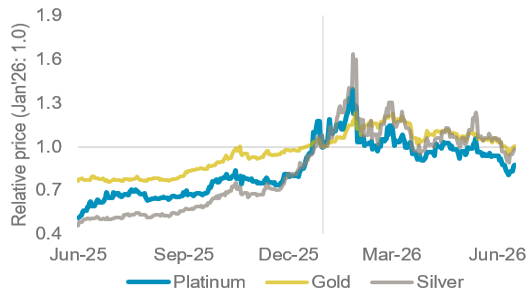

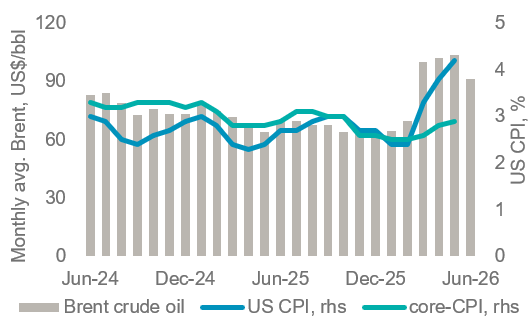

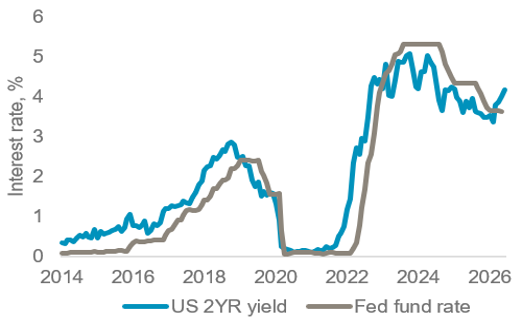

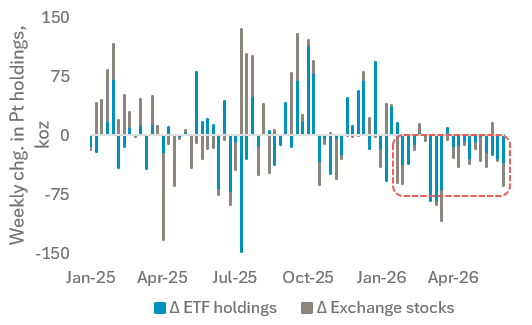

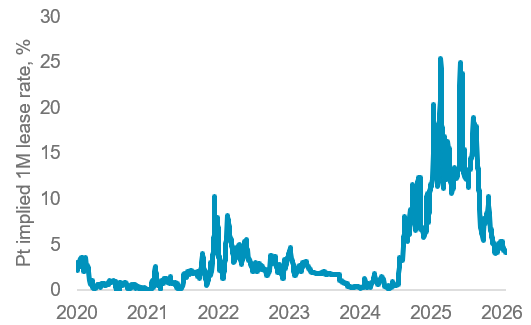

After reaching record price levels in January, the Iran War has been a drag on all precious metals in 2026 (Fig. 2). With the closure of Hormuz, energy led inflation pressure (Fig. 3) is forcing upward revisions to interest rates. US 2-year Treasury yields have risen ~80bps since Mar’26 (Fig. 4) negatively impacting demand for non-yielding assets. In parallel, higher yields have supported US$ appreciation which is negative for commodity prices. The upward bias to interest rate expectations has been compounded by Fed Chair Warsh, who, after his first FOMC meeting cited inflation as a burden, giving no reason not to pursue the reserve’s 2% target (May’26 CPI: 4.2% YoY). Against this backdrop, the platinum price has declined by 17% year-to-date. ETF holdings are -504 koz lower year-to-date and alongside some exchange stock outflows (-240 koz) and strong Q1’26 SA mine supply, physical platinum availability has improved with one-month implied platinum lease rates reaching ~5% during Jun’26 vs. ~15% in Q4’25 (Fig. 6).

Figure 1. ETF holdings have declined by 14% year-to-date

Figure 2. Precious metals prices have declined since Jan’26

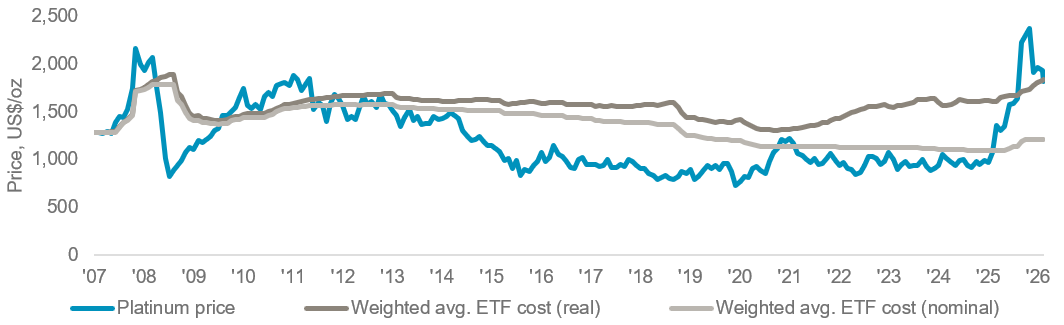

While off from its highs, platinum’s implied lease rate of ~5% is still high by historical standards (Fig. 6). This reflects three years of substantial market deficits with above ground stocks reduced by 60%. ETF outflows YTD have therefore eased but not eliminated market tightness. Indeed, some factors point to platinum’s potential recovery in late 2026. We noted ETF disposals as a headwind, but total holdings of 3,021 koz are at a two-year low and since early 2019, platinum ETF holdings found support at the 3.0 Moz threshold (Fig. 1) which may suggest some sticky ounces. Furthermore, ETF disposals reflect some profit taking and sellers are not price agnostic since investors seek a return (link). We calculate that the current weighted average cost of ETF holdings on a per ounce basis is US$1,800 in real terms (Fig. 7). Accordingly, with a spot platinum price of ~US$1,700/oz, average holdings are no longer in the money.

Finally, if second-order inflationary impacts from energy costs are avoided, the expected rate hikes could be short lived. In the US, core-CPI has increased from 2.5% in Feb’26 to 2.9% in May’26. This indicates that energy inflation has been somewhat contained, albeit FIFA World Cup linked spending may distort summer CPI readings. Monetry policy which ensures a transitory energy shock may allow investors to re-engage in precious metals, including platinum, in late 2026, on or ahead of a return to easing interest rates from 2027.

Platinum’s attraction as an investment asset arises from:

- WPIC research indicates that the platinum market entered a period of consecutive supply deficits from 2023, although a smaller deficit is forecast in 2026 it is not expected to alleviate current market tightness

- Platinum supply remains challenged, materially for mining supply, less so for recycling supply

- Platinum’s end markets are the most diversified of any of the PGMs which is supportive of long-term demand and mitigates future downside risks from external events (Iran War) or structural trends (drivetrain electrification)

- Protracted market deficits have led to elevated lease rates and OTC London backwardation

- The platinum price remains significantly below the price of gold

Figure 3: Higher energy prices have underpinned rising inflation through 2026, albeit core-CPI has yet to meaningfully reflect second-order impacts

Figure 4: With two-year yields typically anticipating Fed decisions, the ~80bps increase in yields since the start of the Iran war suggests the market expects a rate hike

Figure 5: The change in weekly ETF and exchange stock holdings for platinum has largely recorded outflows thus far in 2026

Figure 6: Implied lease rates have declined to mid-single digits on improved availability from investment ounces and mining and recycling supply

Figure 7: Spot platinum prices have crossed below our estimated weighted avg. cost of platinum ETF holdings (in real* terms) which may disincentivise selling

IMPORTANT NOTICE AND DISCLAIMER: This publication is general and solely for educational purposes. The publisher, The World Platinum Investment Council, has been formed by the world’s leading platinum producers to develop the market for platinum investment demand. Its mission is to stimulate investor demand for physical platinum through both actionable insights and targeted development: providing investors with the information to support informed decisions regarding platinum; working with financial institutions and market participants to develop products and channels that investors need.

This publication is not, and should not be construed to be, an offer to sell or a solicitation of an offer to buy any security. With this publication, the publisher does not intend to transmit any order for, arrange for, advise on, act as agent in relation to, or otherwise facilitate any transaction involving securities or commodities regardless of whether such are otherwise referenced in it. This publication is not intended to provide tax, legal, or investment advice and nothing in it should be construed as a recommendation to buy, sell, or hold any investment or security or to engage in any investment strategy or transaction. The publisher is not, and does not purport to be, a broker-dealer, a registered investment advisor, or otherwise registered under the laws of the United States or the United Kingdom, including under the Financial Services and Markets Act 2000 or Senior Managers and Certifications Regime or by the Financial Conduct Authority.

This publication is not, and should not be construed to be, personalized investment advice directed to or appropriate for any particular investor. Any investment should be made only after consulting a professional investment advisor. You are solely responsible for determining whether any investment, investment strategy, security or related transaction is appropriate for you based on your investment objectives, financial circumstances and risk tolerance. You should consult your business, legal, tax or accounting advisors regarding your specific business, legal or tax situation or circumstances.

The information on which this publication is based is believed to be reliable. Nevertheless, the publisher cannot guarantee the accuracy or completeness of the information. This publication contains forward-looking statements, including statements regarding expected continual growth of the industry. The publisher notes that statements contained in the publication that look forward in time, which include everything other than historical information, involve risks and uncertainties that may affect actual results. The logos, services marks and trademarks of the World Platinum Investment Council are owned exclusively by it. All other trademarks used in this publication are the property of their respective trademark holders. The publisher is not affiliated, connected, or associated with, and is not sponsored, approved, or originated by, the trademark holders unless otherwise stated. No claim is made by the publisher to any rights in any third-party trademarks

WPIC Research MiFID II Status

The World Platinum Investment Council -WPIC- has undertaken an internal and external review of its content and services for MiFID II. As a result, WPIC highlights the following to the recipients of its research services, and their Compliance/Legal departments:

WPIC research content falls clearly within the Minor Non-Monetary Benefit Category and can continue to be consumed by all asset managers free of charge. WPIC research can be freely shared across investment organisations.

- WPIC does not conduct any financial instrument execution business. WPIC does not have any market making, sales trading, trading or share dealing activity. (No possible inducement).

- WPIC content is disseminated widely and made available to all interested parties through a range of different channels, therefore qualifying as a “Minor Non-Monetary Benefit” under MiFID II (ESMA/FCA/AMF). WPIC research is made freely available through the WPIC website. WPIC does not have any permissioning requirements on research aggregation platforms.

- WPIC does not, and will not seek, any payment from consumers of our research services. WPIC makes it clear to institutional investors that it does not seek payment from them for our freely available content.

More detailed information is available on the WPIC website:

https://www.platinuminvestment.com/investment-research/mifid-ii

Contacts:

Edward Sterck, Research, [email protected]

Wade Napier, Research, [email protected]

Brendan Clifford, Head of Institutional Distribution, [email protected]

WPIC does not provide investment advice.

Please see disclaimer for more information.