GFEX platinum and palladium futures supporting liquidity and price discovery in China's evolving PGM markets

1 July 2026

Ahead of Shanghai Platinum Week commencing 6 July 2026, it’s worth reflecting on how China’s platinum and palladium markets have responded to the new futures contracts and options on the Guangzhou Futures Exchange (GFEX). GFEX has supported domestic liquidity and improved price discovery with some evidence of a shift away from SGE. From here, we would expect China to play a larger role in global price discovery once GFEX opens access to international participants.

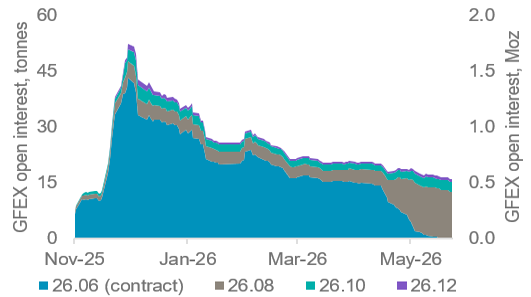

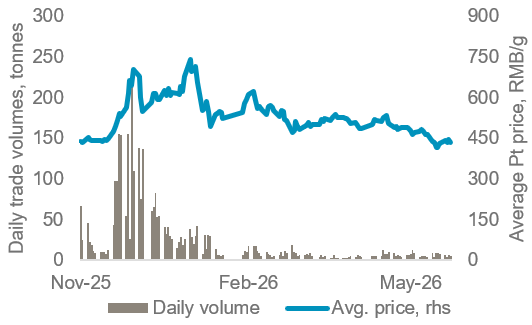

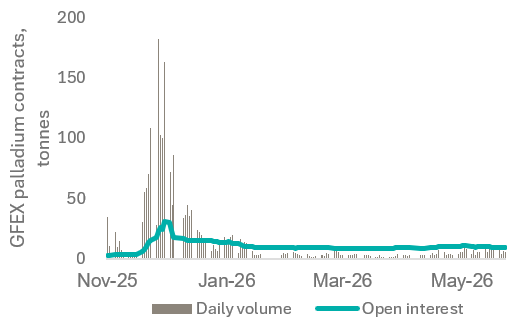

Platinum and palladium futures contracts and options launched on GFEX in Nov’25, with the first contract having expired in Jun’26. Enthusiasm for all precious metals buoyed trading at the end of 2025 and in early 2026 with open interest peaking at 1.7 Moz (52 t) (daily volumes peaked at 7.3 Moz, 228 t). GFEX noted that retail investors accounted for most early volumes. During the initial months of GFEX’s launch, contracts traded at a premium to SGE, which was likely due to overexuberance from retail investors who could not trade on the SGE. From Feb’26, the precious metals rally began easing due to a hawkish Fed chair appointment and Iran war. Through Q2 2026, GFEX open interest moderated and averaged 620 koz (19 t) (Fig. 1) with average daily trade of 186 koz (5.8 t) (Fig. 3). LBMA and NYMEX record average daily volumes of one and two million ounces respectively.

Figure 1. Platinum futures provide significant liquidity

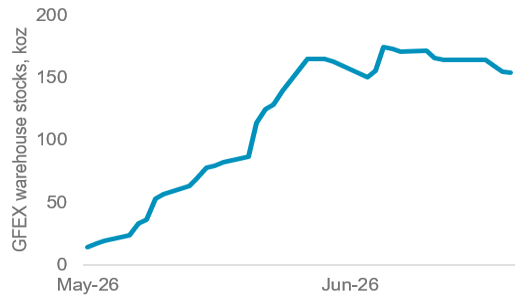

Figure 2. GFEX warehouse stocks have settled above 150 koz

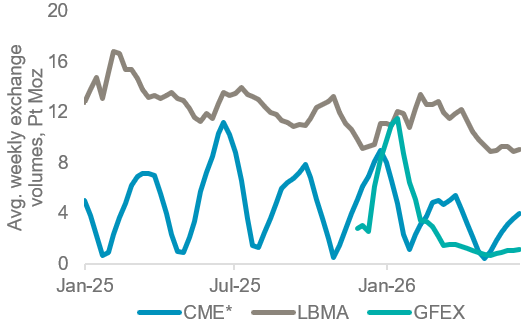

Until GFEX secures Qualified Foreign Investor (QFI) scheme approval arbitraging domestic prices to international benchmarks has been limited to some Chinese institutional investors. Since China is the largest global PGM consumer, it could play a greater role in price discovery if QFI is approved as foreign investors increase GFEX volumes to trade the natural arbitrage across exchanges. The Arbitrage opportunity between exchanges should narrow as participation increases.

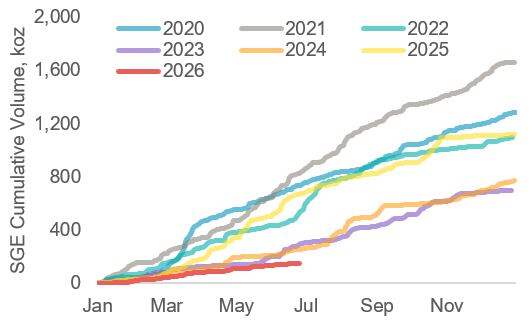

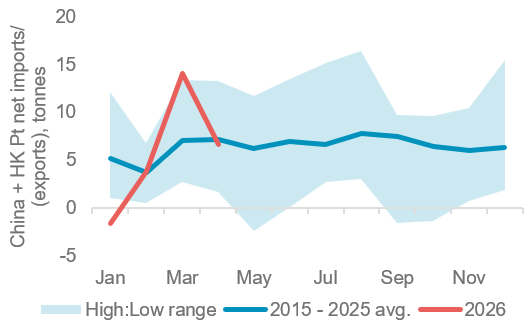

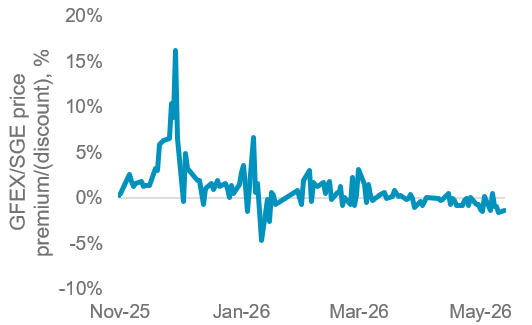

Until then, we are left to assess a largely domestic response to GFEX. SGE volumes have been at their lowest levels this decade during 2026 (Fig. 5) which contrasts with China’s net platinum imports being in-line with historical averages (Fig. 6). Although GFEX contracts allow for physical delivery, it is primarily used for price hedging rather than procurement. The SGE however, only offers one-way trading with physical metal delivery. What is likely happening is that, with GFEX prices beginning to trade at a discount to SGE (Fig. 7), domestic participants are hedging with GFEX while making physical purchases from direct imports or secondary markets such as RTG (both no longer VAT disadvantaged). Chinese imports have also been supported by GFEX exchange stocks building to around 150 koz (4.7t) platinum by Jun’26.

Platinum’s attraction as an investment asset arises from:

- WPIC research indicates that the platinum market entered a period of consecutive supply deficits from 2023 and these are expected to fully deplete above ground stocks by 2029f

- Platinum supply remains challenged, both in terms of primary mining and secondary recycling supply

- Elevated lease rates and OTC London backwardation highlight tight market conditions

- Platinum is a critical mineral in the global energy transition underpinning a key role in the hydrogen economy

- The platinum price remains historically undervalued and significantly below the price of gold

Figure 3: GFEX volumes average 6 tonnes per day in Q2 2026 as initial enthusiasm from retail investors waned from Feb’26 as prices eased

Figure 4: With QFI scheme approval, GFEX volumes are likely to increase as arbitrage opportunities across exchanges become more easily tradeable

Figure 5: Cumulative SGE volumes in 2026 are at their lowest this decade

Figure 6: China’s net platinum imports (incl. HK) to April are in line with average imports over the past ten years

Figure 7: GFEX prices have trended towards a discount to SGE prices

Figure 8: Palladium futures and options contracts have, similarly to platinum, supported domestic liquidity with open interest averaging 9 tonnes during Q2 2026

IMPORTANT NOTICE AND DISCLAIMER: This publication is general and solely for educational purposes. The publisher, The World Platinum Investment Council, has been formed by the world’s leading platinum producers to develop the market for platinum investment demand. Its mission is to stimulate investor demand for physical platinum through both actionable insights and targeted development: providing investors with the information to support informed decisions regarding platinum; working with financial institutions and market participants to develop products and channels that investors need.

This publication is not, and should not be construed to be, an offer to sell or a solicitation of an offer to buy any security. With this publication, the publisher does not intend to transmit any order for, arrange for, advise on, act as agent in relation to, or otherwise facilitate any transaction involving securities or commodities regardless of whether such are otherwise referenced in it. This publication is not intended to provide tax, legal, or investment advice and nothing in it should be construed as a recommendation to buy, sell, or hold any investment or security or to engage in any investment strategy or transaction. The publisher is not, and does not purport to be, a broker-dealer, a registered investment advisor, or otherwise registered under the laws of the United States or the United Kingdom, including under the Financial Services and Markets Act 2000 or Senior Managers and Certifications Regime or by the Financial Conduct Authority.

This publication is not, and should not be construed to be, personalized investment advice directed to or appropriate for any particular investor. Any investment should be made only after consulting a professional investment advisor. You are solely responsible for determining whether any investment, investment strategy, security or related transaction is appropriate for you based on your investment objectives, financial circumstances and risk tolerance. You should consult your business, legal, tax or accounting advisors regarding your specific business, legal or tax situation or circumstances.

The information on which this publication is based is believed to be reliable. Nevertheless, the publisher cannot guarantee the accuracy or completeness of the information. This publication contains forward-looking statements, including statements regarding expected continual growth of the industry. The publisher notes that statements contained in the publication that look forward in time, which include everything other than historical information, involve risks and uncertainties that may affect actual results. The logos, services marks and trademarks of the World Platinum Investment Council are owned exclusively by it. All other trademarks used in this publication are the property of their respective trademark holders. The publisher is not affiliated, connected, or associated with, and is not sponsored, approved, or originated by, the trademark holders unless otherwise stated. No claim is made by the publisher to any rights in any third-party trademarks

WPIC Research MiFID II Status

The World Platinum Investment Council -WPIC- has undertaken an internal and external review of its content and services for MiFID II. As a result, WPIC highlights the following to the recipients of its research services, and their Compliance/Legal departments:

WPIC research content falls clearly within the Minor Non-Monetary Benefit Category and can continue to be consumed by all asset managers free of charge. WPIC research can be freely shared across investment organisations.

- WPIC does not conduct any financial instrument execution business. WPIC does not have any market making, sales trading, trading or share dealing activity. (No possible inducement).

- WPIC content is disseminated widely and made available to all interested parties through a range of different channels, therefore qualifying as a “Minor Non-Monetary Benefit” under MiFID II (ESMA/FCA/AMF). WPIC research is made freely available through the WPIC website. WPIC does not have any permissioning requirements on research aggregation platforms.

- WPIC does not, and will not seek, any payment from consumers of our research services. WPIC makes it clear to institutional investors that it does not seek payment from them for our freely available content.

More detailed information is available on the WPIC website:

https://www.platinuminvestment.com/investment-research/mifid-ii

Contacts:

Edward Sterck, Research, [email protected]

Wade Napier, Research, [email protected]

Brendan Clifford, Head of Institutional Distribution, [email protected]

WPIC does not provide investment advice.

Please see disclaimer for more information.