PEM capacity growth revised downward in IEA update, dampening platinum demand despite rising electrolysis

6 January 2026

The International Energy Agency’s (IEA) annual outlook for hydrogen electrolyser projects in 2025 shows an evolving landscape. The most significant changes are to the number of pre-2030f projects being deferred to post-2030 and a mild technology shift towards alkaline. Accordingly, platinum demand from electrolysis from 2026f to 2030f is expected to be 12% lower than in our projections last year, reaching 172 koz p.a. by the end of the decade.

The IEA hydrogen production projects database details operational and proposed electrolyser plans globally. The database is updated annually, with the following key highlights from the 2025 edition (relative 2024).

· The total number of hydrogen projects expected to be commissioned by 2040f has increased by 9% (Fig. 3),

· The cumulative electrolyser capacity has increased by 8% (Fig. 4) due to a greater number of projects, however

· Average project sizes have declined by 1%.

Despite the IEA recording growing electrolysis ambitions, green hydrogen continues to face implementation headwinds stemming from high costs, regulatory uncertainty and infrastructure bottlenecks. Recognising these challenges WPIC applies a probability success factor against the IEA project list to reflect the likelihood that a project reaches commissioning. The less advanced a project’s status is (e.g. conceptual study versus construction phase), the lower the likelihood it successfully commissions.

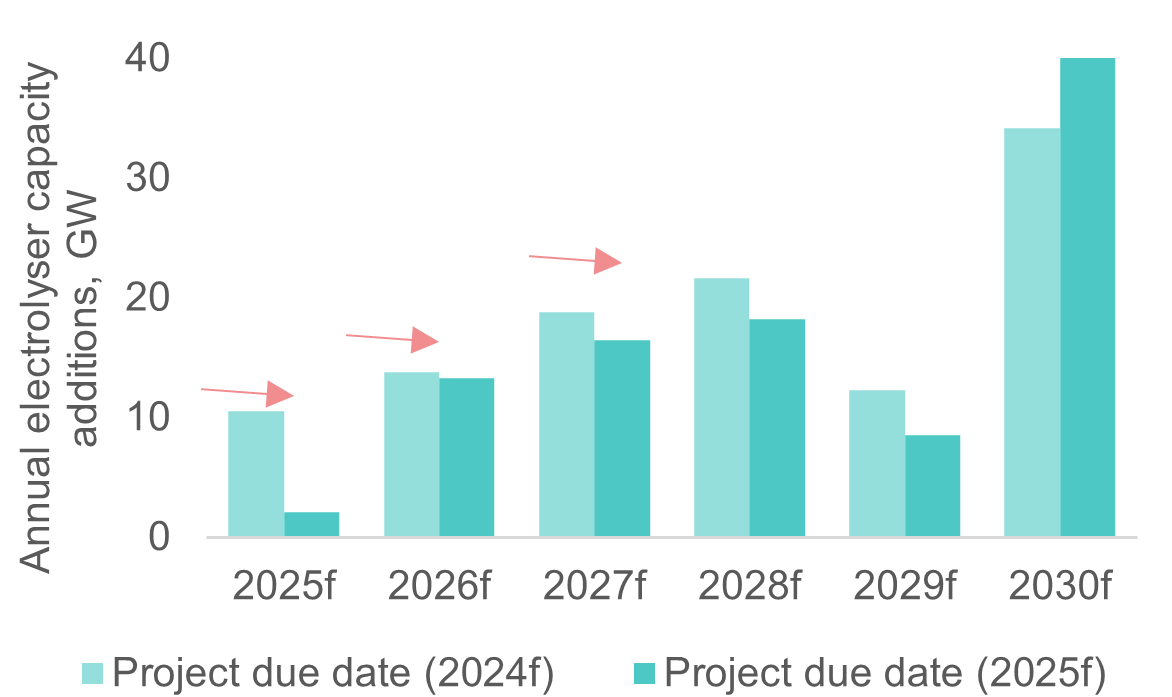

Figure 1. Projects deferrals see near-term downgrades partially offset by longer term upgrades

Figure 2. Near-term platinum demand declines with PEM, rebounding by 2030 as deferred projects come online

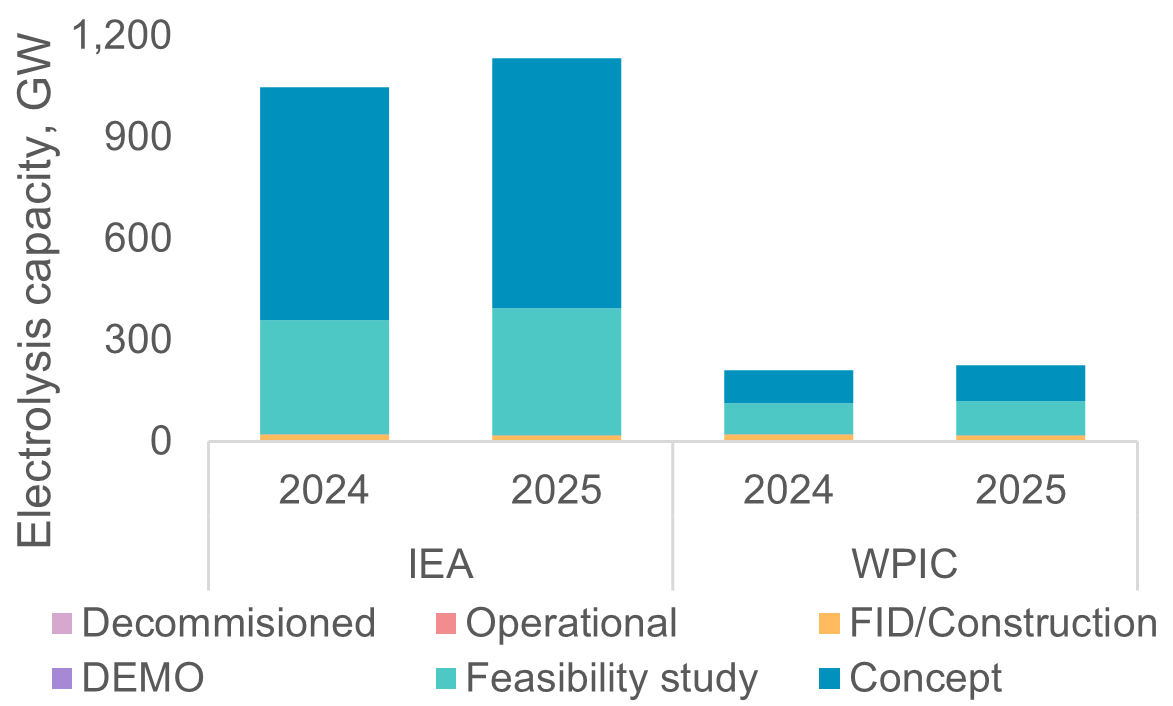

After applying these weightings, WPIC expects total cumulative electrolysis capacity to reach 225 GW by 2040f, a 6% increase versus the 2024 database, but well below the ~1,100 GW of project capacity listed by the IEA (Fig. 4). The upward revisions to total electrolyser capacity masks trends across pre- and post-2030f time frames. Due to ongoing industry challenges, electrolysis capacity forecasts have been reduced by 24% from 2025f to 2029f (Fig. 1) as projects are deferred or cancelled.

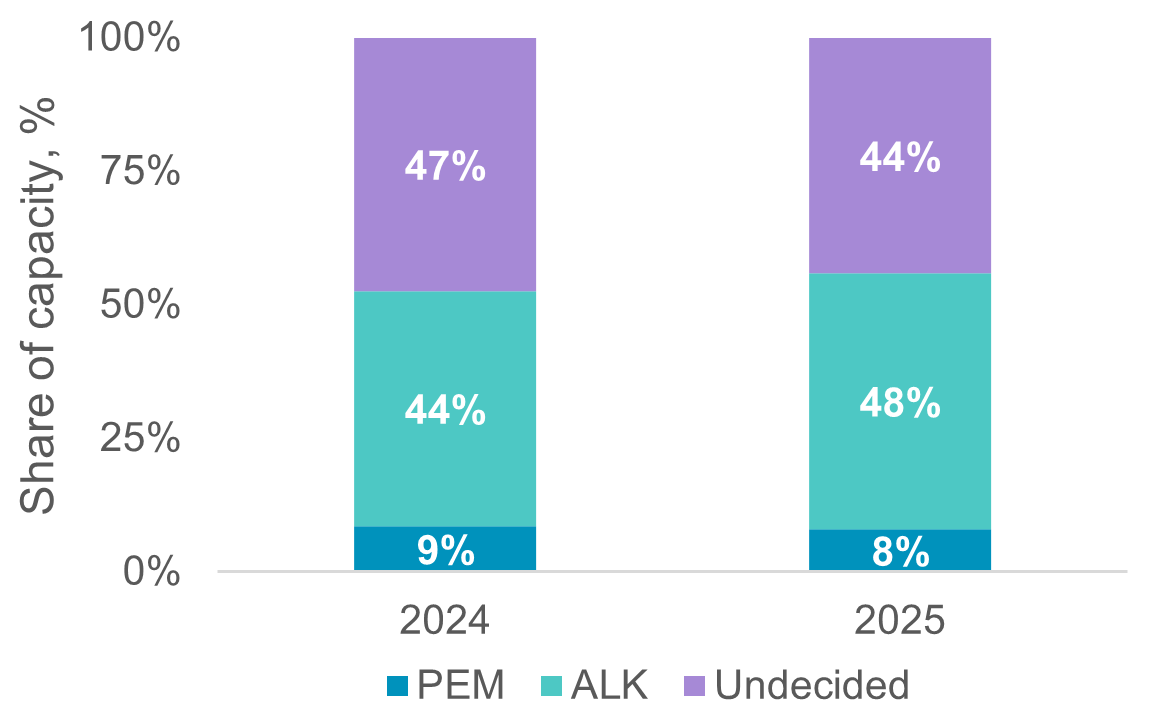

In addition to project timelines, the IEA database shows evolving electrolysis technology preferences. The revised databased highlights a rising relative proportion alkaline adoption, stable PEM adoption and a declining proportion of unallocated technology choices (Fig. 6). This suggests that a growing portion projects with undecided technology may adopt alkaline which mostly do not use PGMs. We expect this technology shift combined with medium-term project deferrals to reduce platinum demand by 12% from 2026f to 2030f (Fig. 2). Hydrogen in totality remains a compelling growth story with the segment accounting for <1% of total platinum demand in 2025f but increasing to 4% by 2030f.

Platinum’s attraction as an investment asset arises from:

- WPIC research indicates that the platinum market entered a period of consecutive supply deficits from 2023, although a balanced market is forecast in 2026 it is not expected to alleviate current market tightness

- Platinum supply remains challenged, both in terms of primary mining and secondary recycling supply

- Although US tariffs present some downside risks to demand, these are likely offset by tailwinds to jewellery demand and Chinese investment demand

- Elevated lease rates and OTC London backwardation highlight tight market conditions

- The platinum price remains significantly below the price of gold

Figure 3: Total announced projects are up 9% YoY

Figure 4: IEA announced project capacity is up 8% YoY, WPIC probability adjusted built* capacity is up 6% YoY

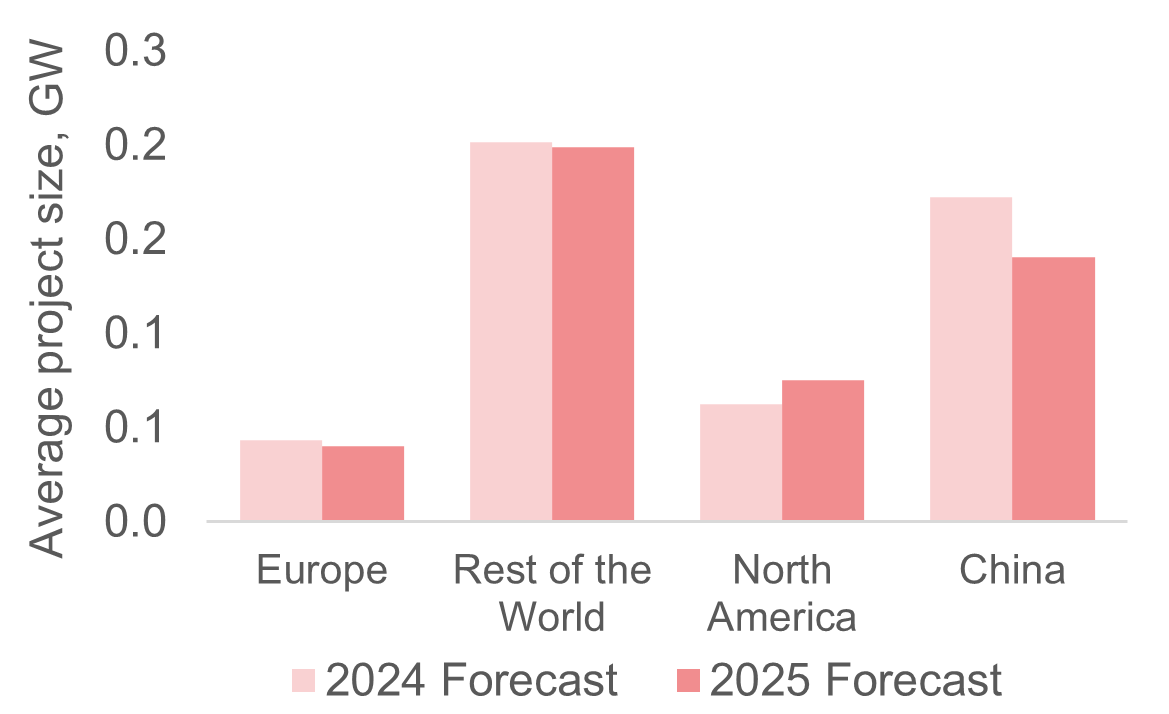

Figure 5: Average probability adjusted individual project sizes have decreased by 5%, with RoW hosting the largest projects and Europe the smallest

Figure 6: The share of alkaline electrolysis to 2030 has increased by 4% reducing PEM market share

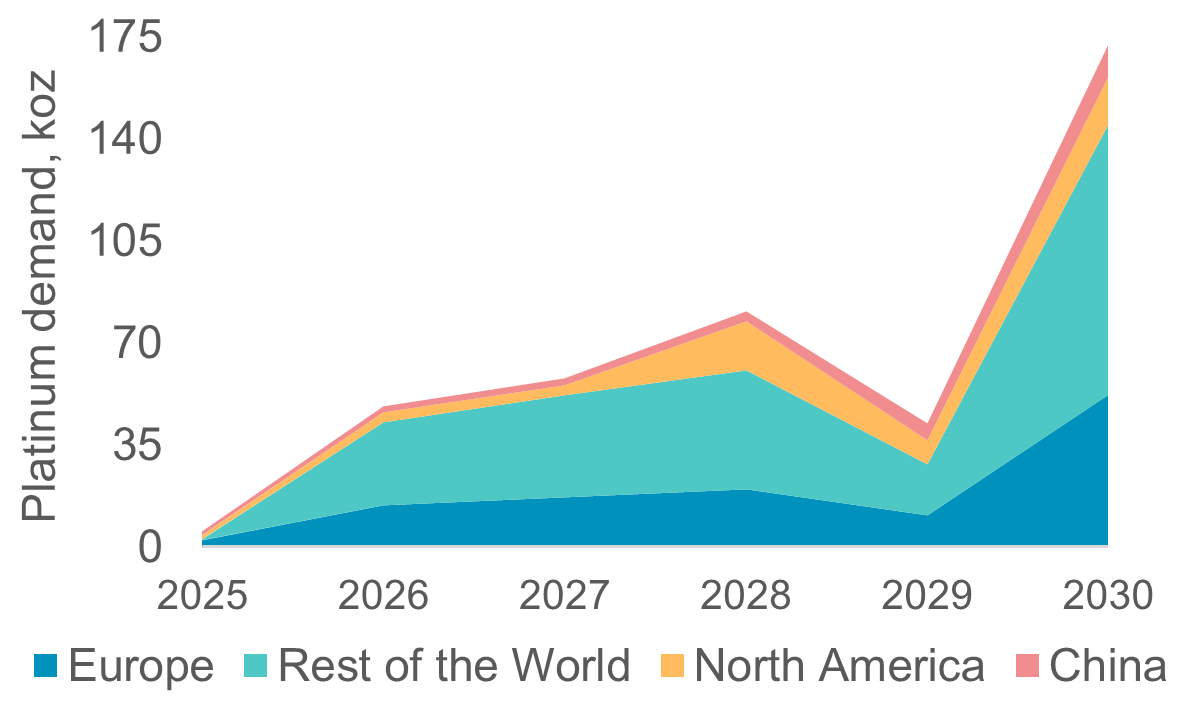

Figure 7: Most electrolysis platinum demand is expected to come from Europe and Rest of the World, making up ~81% of cumulative platinum demand

Figure 8: Overall, this has pushed ‘hydrogen stationary and other’ platinum demand out to 2030f to 312 koz, accounting for ~70% of platinum demand from hydrogen

IMPORTANT NOTICE AND DISCLAIMER: This publication is general and solely for educational purposes. The publisher, The World Platinum Investment Council, has been formed by the world’s leading platinum producers to develop the market for platinum investment demand. Its mission is to stimulate investor demand for physical platinum through both actionable insights and targeted development: providing investors with the information to support informed decisions regarding platinum; working with financial institutions and market participants to develop products and channels that investors need.

This publication is not, and should not be construed to be, an offer to sell or a solicitation of an offer to buy any security. With this publication, the publisher does not intend to transmit any order for, arrange for, advise on, act as agent in relation to, or otherwise facilitate any transaction involving securities or commodities regardless of whether such are otherwise referenced in it. This publication is not intended to provide tax, legal, or investment advice and nothing in it should be construed as a recommendation to buy, sell, or hold any investment or security or to engage in any investment strategy or transaction. The publisher is not, and does not purport to be, a broker-dealer, a registered investment advisor, or otherwise registered under the laws of the United States or the United Kingdom, including under the Financial Services and Markets Act 2000 or Senior Managers and Certifications Regime or by the Financial Conduct Authority.

This publication is not, and should not be construed to be, personalized investment advice directed to or appropriate for any particular investor. Any investment should be made only after consulting a professional investment advisor. You are solely responsible for determining whether any investment, investment strategy, security or related transaction is appropriate for you based on your investment objectives, financial circumstances and risk tolerance. You should consult your business, legal, tax or accounting advisors regarding your specific business, legal or tax situation or circumstances.

The information on which this publication is based is believed to be reliable. Nevertheless, the publisher cannot guarantee the accuracy or completeness of the information. This publication contains forward-looking statements, including statements regarding expected continual growth of the industry. The publisher notes that statements contained in the publication that look forward in time, which include everything other than historical information, involve risks and uncertainties that may affect actual results. The logos, services marks and trademarks of the World Platinum Investment Council are owned exclusively by it. All other trademarks used in this publication are the property of their respective trademark holders. The publisher is not affiliated, connected, or associated with, and is not sponsored, approved, or originated by, the trademark holders unless otherwise stated. No claim is made by the publisher to any rights in any third-party trademarks

WPIC Research MiFID II Status

The World Platinum Investment Council -WPIC- has undertaken an internal and external review of its content and services for MiFID II. As a result, WPIC highlights the following to the recipients of its research services, and their Compliance/Legal departments:

WPIC research content falls clearly within the Minor Non-Monetary Benefit Category and can continue to be consumed by all asset managers free of charge. WPIC research can be freely shared across investment organisations.

- WPIC does not conduct any financial instrument execution business. WPIC does not have any market making, sales trading, trading or share dealing activity. (No possible inducement).

- WPIC content is disseminated widely and made available to all interested parties through a range of different channels, therefore qualifying as a “Minor Non-Monetary Benefit” under MiFID II (ESMA/FCA/AMF). WPIC research is made freely available through the WPIC website. WPIC does not have any permissioning requirements on research aggregation platforms.

- WPIC does not, and will not seek, any payment from consumers of our research services. WPIC makes it clear to institutional investors that it does not seek payment from them for our freely available content.

More detailed information is available on the WPIC website:

https://www.platinuminvestment.com/investment-research/mifid-ii

Contacts:

Edward Sterck, Research, [email protected]

Wade Napier, Research, [email protected]

Brendan Clifford, Head of Institutional Distribution, [email protected]

WPIC does not provide investment advice.

Please see disclaimer for more information.