Revised US emission timelines support higher for longer PGM demand

28 March 2024

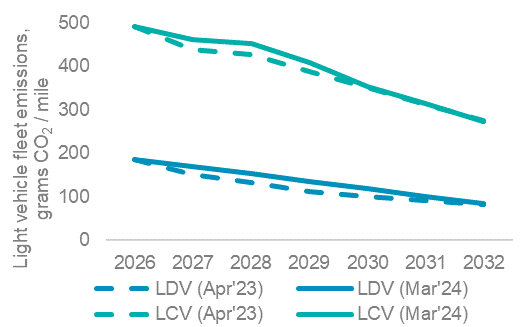

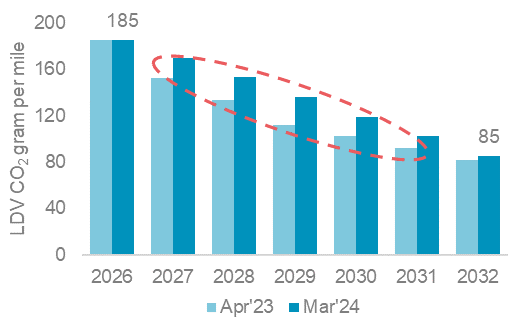

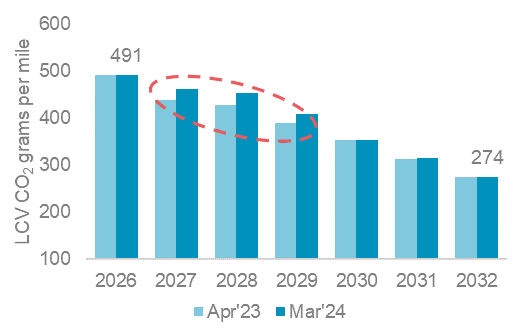

The United States has finalised its vehicle emission reduction targets for 2032. The Environmental Protection Agency (EPA) has set CO2 emission reduction targets of -56% and -44% for light-duty and light-commercial vehicles respectively between 2026 and 2032. These targets are unchanged from those proposed in April 2023, however, the interim thresholds leading up to the 2032 targets have been made more lenient, thereby allowing for a slower initial BEV transition (Fig. 1). WPIC estimates that each 1% of North American ICE-based market share supports around 25 koz of 2E PGM demand respectively.

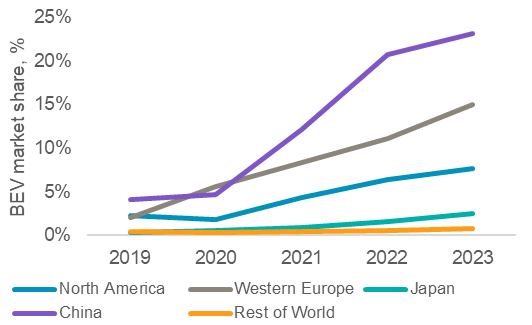

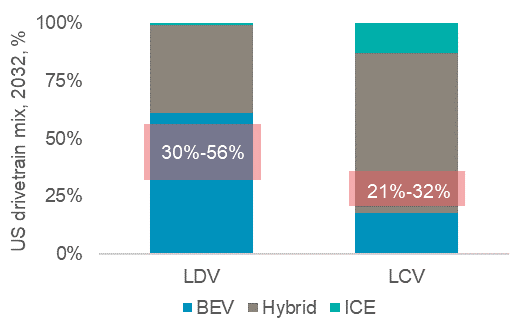

The US utilises fleet average emission standards which means an automaker’s fleet (as a ratio of sales volumes) must comply with emission thresholds rather than any single vehicle. The technology agnostic approach allows a varying drivetrain split between ICE, hybrid, fuel cell and electric. The EPA estimates that by 2032, BEV market share (Fig. 7) will range between 30-56% for LDV (WPIC: 61%) and between 20-32% for LCV (WPIC: 18%). While the 2032 targets appear reasonable, flexibility is important to a US consumer that currently favours large combustion engine vehicles. US BEV market share reached 8% in 2023, lagging China and Europe at 23% and 15% respectively (Fig. 4). The Inflation Reduction Act (IRA) should help US BEV adoption; however, investment will only see results over the medium-term. Hence, the EPA’s decision to revise interim fleet average emission thresholds (Fig. 1) lowers the near-term pressure on automakers to push consumers to switch to BEV and allows more ICE-based vehicle sales in the US.

Figure 1: The changes announced by the EPA allow for more lenient interim emission thresholds

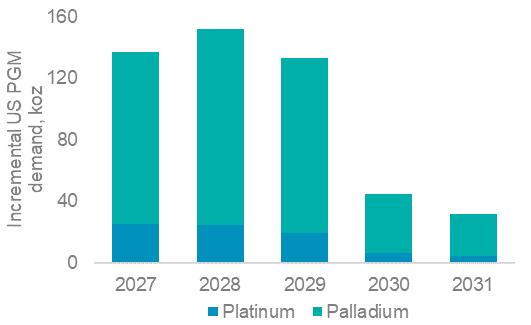

Figure 2: PGM demand could benefit from less stringent regulation allowing for higher PGM containing ICE sales

WPIC estimates the US could sell a cumulative three million additional ICE-based light-vehicles between 2027 and 2031, which is an additional 100 koz 2E PGM p.a. on average (Fig. 2). On a standalone basis, 100 koz of 2E PGM is 0.5% of incremental 2E demand. However, the more important take away is the growing global trend of concessions to emission reduction timelines which cumulatively extends the role of ICE. During 2023,

• The UK deferred its ban on ICE vehicle sales by five years,

• The EU approved the post-2035 sale of e-fuelled ICE vehicles, and

• Several automakers re-prioritised hybrids in future model rollouts.

Furthermore, protectionist overtures against Chinese vehicle imports may protect EU and US automakers (plus their workforces) whose vehicle mix is skewed to ICE powertrains. These multi-faceted considerations suggest hybrid vehicles have a core role in decarbonising transport. Accordingly, despite rising BEV market share, an automotive PGM demand decline will be moderate at -1.2% CAGR between 2023 and 2028 (Fig. 8).

Platinum’s attraction as an investment asset arises from:

- WPIC research indicates the platinum market entering a period of consecutive deficits from 2023.

- Platinum supply remains challenged, hampered by production challenges in South Africa and with recycling supplies.

- Automotive platinum demand growth should continue due principally to substitution in gasoline vehicles.

- Growing off a small base, hydrogen will be a major source of platinum demand in the future.

- The platinum price remains historically undervalued and significantly below both gold and palladium.

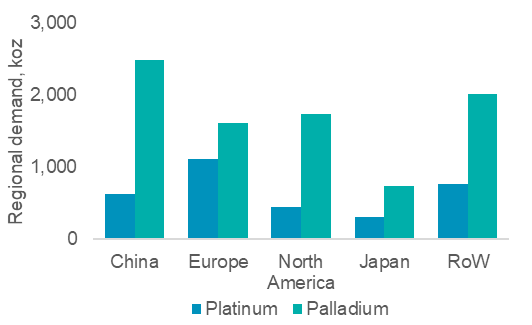

Figure 3: North America is the third largest end market for automotive PGM demand, 2023

Figure 4: North American BEV market share lags China and Europe

Figure 5: Interim fleet average emission targets for light-duty vehicles have been made more lenient by the US EPA

Figure 6: Interim fleet average emission targets for light commercial vehicles have also been made more lenient by the US EPA

Figure 7: The EPA’s estimated BEV market shares by 2032 are between 30-56% for LDV (WPIC: 61%) and between 20-32% for LCV (WPIC: 18%)

Figure 8: Hybridisation of the drivetrain will support automotive PGM demand despite rising BEV market share

IMPORTANT NOTICE AND DISCLAIMER: This publication is general and solely for educational purposes. The publisher, The World Platinum Investment Council, has been formed by the world’s leading platinum producers to develop the market for platinum investment demand. Its mission is to stimulate investor demand for physical platinum through both actionable insights and targeted development: providing investors with the information to support informed decisions regarding platinum; working with financial institutions and market participants to develop products and channels that investors need.

This publication is not, and should not be construed to be, an offer to sell or a solicitation of an offer to buy any security. With this publication, the publisher does not intend to transmit any order for, arrange for, advise on, act as agent in relation to, or otherwise facilitate any transaction involving securities or commodities regardless of whether such are otherwise referenced in it. This publication is not intended to provide tax, legal, or investment advice and nothing in it should be construed as a recommendation to buy, sell, or hold any investment or security or to engage in any investment strategy or transaction. The publisher is not, and does not purport to be, a broker-dealer, a registered investment advisor, or otherwise registered under the laws of the United States or the United Kingdom, including under the Financial Services and Markets Act 2000 or Senior Managers and Certifications Regime or by the Financial Conduct Authority.

This publication is not, and should not be construed to be, personalized investment advice directed to or appropriate for any particular investor. Any investment should be made only after consulting a professional investment advisor. You are solely responsible for determining whether any investment, investment strategy, security or related transaction is appropriate for you based on your investment objectives, financial circumstances and risk tolerance. You should consult your business, legal, tax or accounting advisors regarding your specific business, legal or tax situation or circumstances.

The information on which this publication is based is believed to be reliable. Nevertheless, the publisher cannot guarantee the accuracy or completeness of the information. This publication contains forward-looking statements, including statements regarding expected continual growth of the industry. The publisher notes that statements contained in the publication that look forward in time, which include everything other than historical information, involve risks and uncertainties that may affect actual results. The logos, services marks and trademarks of the World Platinum Investment Council are owned exclusively by it. All other trademarks used in this publication are the property of their respective trademark holders. The publisher is not affiliated, connected, or associated with, and is not sponsored, approved, or originated by, the trademark holders unless otherwise stated. No claim is made by the publisher to any rights in any third-party trademarks

WPIC Research MiFID II Status

The World Platinum Investment Council -WPIC- has undertaken an internal and external review of its content and services for MiFID II. As a result, WPIC highlights the following to the recipients of its research services, and their Compliance/Legal departments:

WPIC research content falls clearly within the Minor Non-Monetary Benefit Category and can continue to be consumed by all asset managers free of charge. WPIC research can be freely shared across investment organisations.

- WPIC does not conduct any financial instrument execution business. WPIC does not have any market making, sales trading, trading or share dealing activity. (No possible inducement).

- WPIC content is disseminated widely and made available to all interested parties through a range of different channels, therefore qualifying as a “Minor Non-Monetary Benefit” under MiFID II (ESMA/FCA/AMF). WPIC research is made freely available through the WPIC website. WPIC does not have any permissioning requirements on research aggregation platforms.

- WPIC does not, and will not seek, any payment from consumers of our research services. WPIC makes it clear to institutional investors that it does not seek payment from them for our freely available content.

More detailed information is available on the WPIC website:

https://www.platinuminvestment.com/investment-research/mifid-ii

Contacts:

Edward Sterck, Research, [email protected]

Wade Napier, Research, [email protected]

Brendan Clifford, Head of Institutional Distribution, [email protected]

WPIC does not provide investment advice.

Please see disclaimer for more information.