The Iran War’s direct impact on platinum demand appears modest, but higher interest rate expectations and a stronger US dollar could weigh on investment demand

2 April 2026

The Iran war has entered its second month. Iran and the broader Middle East (ME) are not large direct markets for platinum supply and demand. Contagion impacts currently appear more likely from the economic drag caused by restrictions across the Strait of Hormuz and the potential for a global helium shortage to impact semiconductor production (which may impact vehicle production). While the second order impacts to platinum’s fundamentals appear modest, at this time, the primary risk to demand stems from the potential for investors to liquidate positions as rising interest rate expectations and a recovering US dollar weigh on broader metals prices.

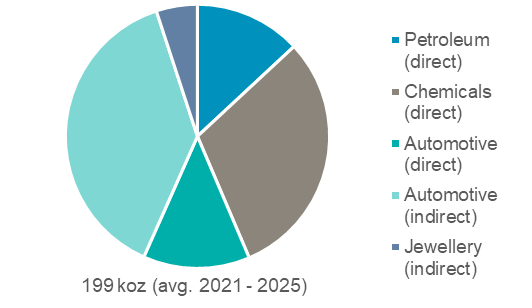

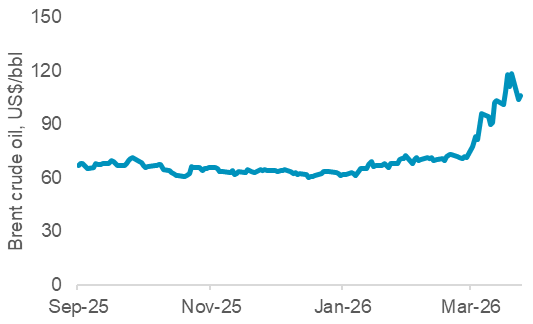

We estimate the ME accounts for around 2.5% of global platinum demand or ~200 koz pa (Fig. 1). Direct platinum demand is around 110 koz pa from vehicle production of ~1M units, and chemical and petroleum market shares of ~10% and 15% respectively. Indirect platinum demand of ~90 koz pa stems from vehicle imports of 2-3M units and jewellery imports. While a protracted conflict would invariably negatively impact some platinum demand tied to the ME, the impact of restricting the Strait of Hormuz and higher energy prices (Fig. 3) may have a greater impact on platinum markets.

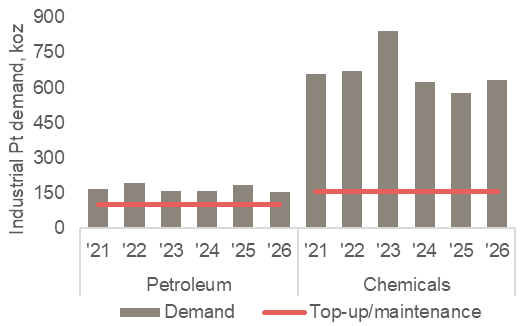

Around 20% of global crude and LNG output flows via the Strait. Without these feedstocks for petroleum refining and chemicals sectors, utilisation rates decline and some maintenance is deferred. We estimate global platinum top-up requirements for the petroleum and chemicals markets is around 250 koz pa. (Fig. 4). Simplistically, losing 20% of annual feedstock supply could imply a 50 koz reduction in platinum top-up needs.

Figure 1. Middle Eastern platinum demand is ~200 koz pa

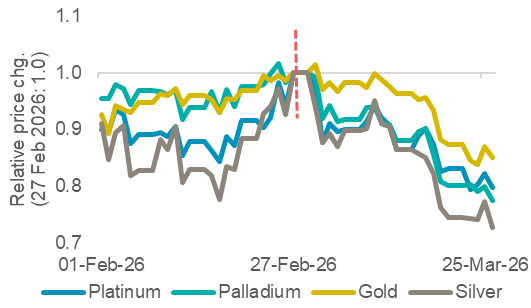

Figure 2. The Iran War has led precious metals prices lower

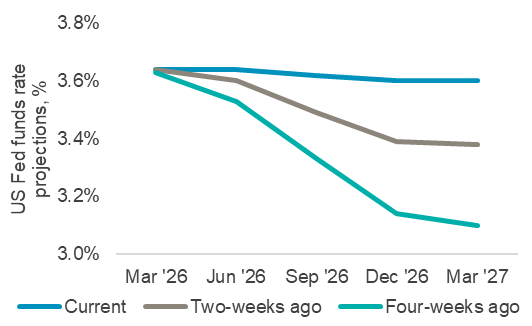

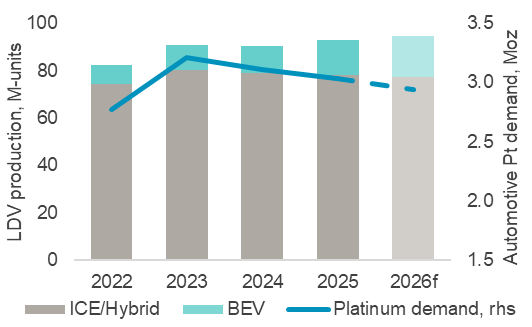

Three factors may weigh on automotive demand. Firstly, higher oil prices might prompt switching from ICE vehicles to BEVs (ignoring higher upfront costs and that electricity prices are also likely to rise). Each 1% gain in BEV market share reduces platinum demand by ~25 koz. Secondly, with higher energy prices being inflationary, rate setting expectations for the US Fed are revised from two cuts to none in 2026f (Fig. 5). Higher finance costs could lead to deferred new car purchases. Our March Platinum Quarterly (link) assumed light-duty (LDV) production would increase by 2% YoY to 95M units in 2026f (Fig. 6). Platinum demand could be impacted by -35 koz in 2026f, if economic conditions inhibit LDV growth. Finally, restrictions to Qatar’s helium exports (~30% global supply) could impact semiconductor manufacturing and in turn vehicle production (reminiscent of 2021/22).

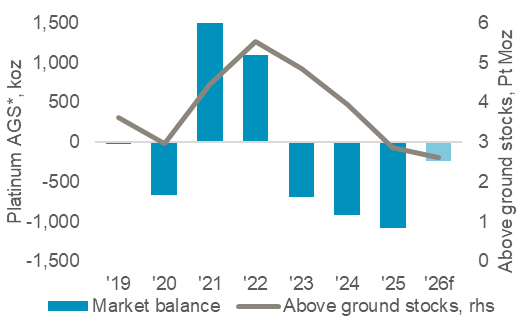

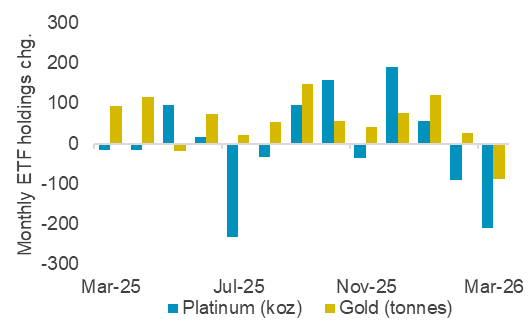

We currently do not believe that auto or industrial platinum demand would cumulatively reduce enough to erode our current deficit of 240 koz in 2026f (Fig. 7). However, recent investor positioning has been more impactful. In March 2026, platinum ETF holdings declined by 224 koz (Fig. 8) as the broader precious metals complex saw prices decrease ~20% (Fig. 2) on higher interest rate expectations and US$ strength.

Platinum’s attraction as an investment asset arises from:

- WPIC research indicates that the platinum market entered a period of consecutive supply deficits from 2023, although a smaller deficit is forecast in 2026 it is not expected to alleviate current market tightness

- Platinum supply remains challenged, materially for mining supply, less so for recycling supply

- Platinum’s end markets are the most diversified of PGMs which is supportive of long-term demand and mitigates future downside risks from external events (Iran War) or structural trends (drivetrain electrification)

- Elevated lease rates and OTC London backwardation highlight sustained tight market conditions

- The platinum price remains significantly below the price of gold

Figure 3: The Brent crude oil price has increased by approximately 60% since the start of the Iran War on 28 February 2026

Figure 4: On an annualised basis, installed petroleum refining and chemicals infrastructure requires around 250 koz pa of platinum for catalyst maintenance purposes

Figure 5: The number of projected US Fed interest rate cuts in 2026 has declined since the start of the Iran War due to higher inflation expectations

Figure 6: The war could slow LDV production, however, an accelerated transition to BEV appears unlikely since hybrids similarly help mitigate higher fuel costs

Figure 7: The cumulative impacts to platinum automotive and industrial demand are unlikely to completely erode a fourth consecutive year of platinum market deficits

Figure 8: The second order effects that the Iran War has had on interest rate expectations has led investors to liquidate some ETF holdings in March 2026

IMPORTANT NOTICE AND DISCLAIMER: This publication is general and solely for educational purposes. The publisher, The World Platinum Investment Council, has been formed by the world’s leading platinum producers to develop the market for platinum investment demand. Its mission is to stimulate investor demand for physical platinum through both actionable insights and targeted development: providing investors with the information to support informed decisions regarding platinum; working with financial institutions and market participants to develop products and channels that investors need.

This publication is not, and should not be construed to be, an offer to sell or a solicitation of an offer to buy any security. With this publication, the publisher does not intend to transmit any order for, arrange for, advise on, act as agent in relation to, or otherwise facilitate any transaction involving securities or commodities regardless of whether such are otherwise referenced in it. This publication is not intended to provide tax, legal, or investment advice and nothing in it should be construed as a recommendation to buy, sell, or hold any investment or security or to engage in any investment strategy or transaction. The publisher is not, and does not purport to be, a broker-dealer, a registered investment advisor, or otherwise registered under the laws of the United States or the United Kingdom, including under the Financial Services and Markets Act 2000 or Senior Managers and Certifications Regime or by the Financial Conduct Authority.

This publication is not, and should not be construed to be, personalized investment advice directed to or appropriate for any particular investor. Any investment should be made only after consulting a professional investment advisor. You are solely responsible for determining whether any investment, investment strategy, security or related transaction is appropriate for you based on your investment objectives, financial circumstances and risk tolerance. You should consult your business, legal, tax or accounting advisors regarding your specific business, legal or tax situation or circumstances.

The information on which this publication is based is believed to be reliable. Nevertheless, the publisher cannot guarantee the accuracy or completeness of the information. This publication contains forward-looking statements, including statements regarding expected continual growth of the industry. The publisher notes that statements contained in the publication that look forward in time, which include everything other than historical information, involve risks and uncertainties that may affect actual results. The logos, services marks and trademarks of the World Platinum Investment Council are owned exclusively by it. All other trademarks used in this publication are the property of their respective trademark holders. The publisher is not affiliated, connected, or associated with, and is not sponsored, approved, or originated by, the trademark holders unless otherwise stated. No claim is made by the publisher to any rights in any third-party trademarks

WPIC Research MiFID II Status

The World Platinum Investment Council -WPIC- has undertaken an internal and external review of its content and services for MiFID II. As a result, WPIC highlights the following to the recipients of its research services, and their Compliance/Legal departments:

WPIC research content falls clearly within the Minor Non-Monetary Benefit Category and can continue to be consumed by all asset managers free of charge. WPIC research can be freely shared across investment organisations.

- WPIC does not conduct any financial instrument execution business. WPIC does not have any market making, sales trading, trading or share dealing activity. (No possible inducement).

- WPIC content is disseminated widely and made available to all interested parties through a range of different channels, therefore qualifying as a “Minor Non-Monetary Benefit” under MiFID II (ESMA/FCA/AMF). WPIC research is made freely available through the WPIC website. WPIC does not have any permissioning requirements on research aggregation platforms.

- WPIC does not, and will not seek, any payment from consumers of our research services. WPIC makes it clear to institutional investors that it does not seek payment from them for our freely available content.

More detailed information is available on the WPIC website:

https://www.platinuminvestment.com/investment-research/mifid-ii

Contacts:

Edward Sterck, Research, [email protected]

Wade Napier, Research, [email protected]

Brendan Clifford, Head of Institutional Distribution, [email protected]

WPIC does not provide investment advice.

Please see disclaimer for more information.