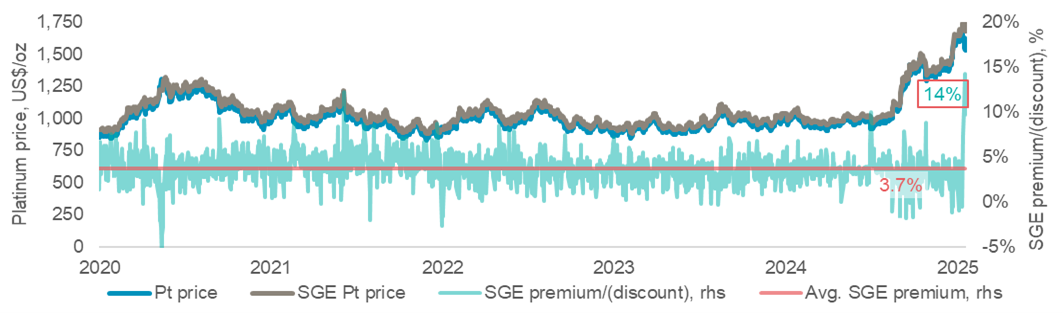

22 October 2025: The removal of VAT exemptions on platinum imports will increase the cost of platinum in China: The removal of VAT exemptions on platinum imports will increase the cost of platinum in China: China has announced amendments to Value-Added Tax (VAT) policies. The amendments include the cancellation of the 13% VAT exemption on platinum imports from 1 November 2025. Cancelling platinum imports’ VAT exemption will put upward pressure on Shanghai Gold Exchange (SGE) platinum quotes which may, in turn, negatively impact China’s historically price sensitive platinum demand.

Platinum Perspectives

WPIC® research is free of charge. It can be consumed by asset managers under MiFID II

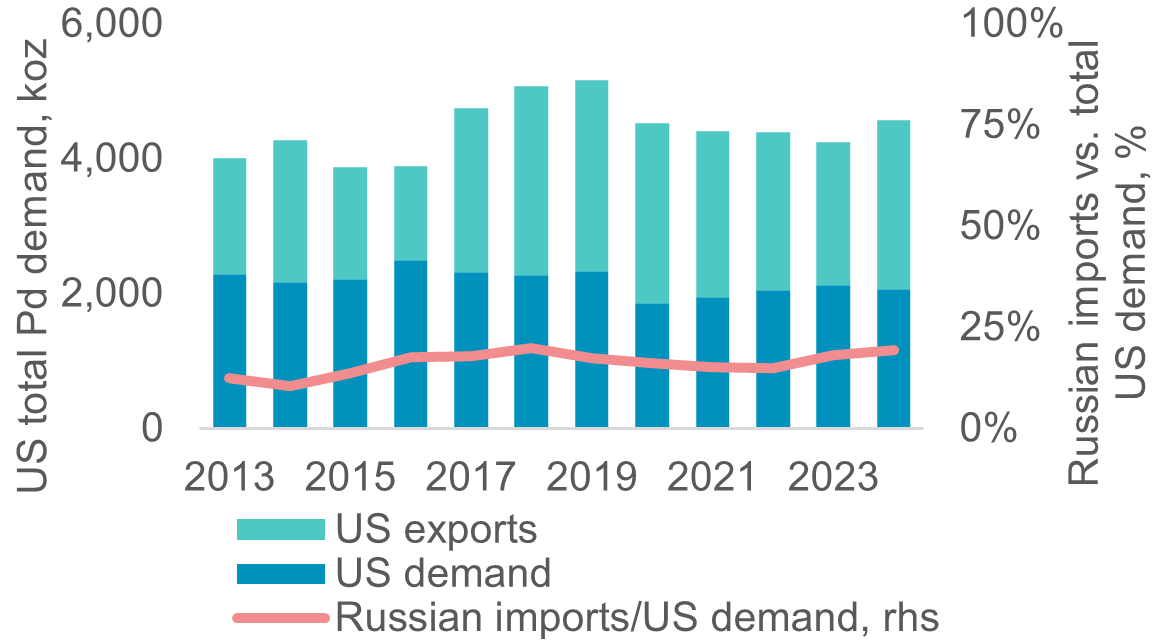

17 October 2025: US trade action on Russian palladium aims to protect domestic producers but may tighten supply and lift prices: US trade action on Russian palladium aims to protect domestic producers but may tighten supply and lift prices: Sibanye-Stillwater together with the United Steelworkers union have filed antidumping and countervailing duty petitions against Russian unwrought palladium imports. Duties on Russian palladium will likely restrict imports and tighten domestic markets since higher US domestic production and trade re-routing will take time to implement. Accordingly, US palladium prices could experience some continued upward pressure on exacerbated trade restrictions.

12 August 2025: Platinum ETF selling after c.50% price increase, offset by strength in bar and coin, jewellery, and exchange stocks: Platinum ETF selling after c.50% price increase, offset by strength in bar and coin, jewellery, and exchange stocks: The strong year-to-date platinum price increase of ~50% has led to some selling by exchange traded fund (ETF) investors. In our view, ETF outflows are unlikely to materially narrow the substantial platinum market deficit forecast for 2025 since, 1) Chinese jewellery and bar and coin investment demand has been stronger than anticipated through H1 2025 and 2) tariff risks have led to a re-accumulation of metal into NYMEX exchange stocks.

5 August 2025: Deregulating US emissions legislation intends to remove EV mandates and should not negatively impact PGMs: Deregulating US emissions legislation intends to remove EV mandates and should not negatively impact PGMs: The US’ Environmental Protection Agency (with probable Whitehouse influence) has proposed repealing greenhouse gas emissions standards for vehicles. Our view is that these actions reflect moves against electric vehicle mandating, further slowing BEV adoption, but with the agency simultaneously noting that legislation regulating criteria pollutants (NOx, CO, etc.) will be unaffected. Accordingly, as catalytic convertors support the reduction of criteria pollutants, PGM demand should be unaffected.

29 July 2025: Platinum market tightness persists, despite ETF and exchange stock outflows: Platinum market tightness persists, despite ETF and exchange stock outflows: The over 50% year-to-date increase in the platinum price, together with easing tariff fears (albeit temporary) have resulted in almost 300 koz coming out of ETFs and exchange stocks, since the start of Q2 2025. Despite this significant injection of metal supply, lease rates remain elevated. Strong imports into China and some reemergence of tariff risks are keeping markets tight. At current prices, this may only be solved by a shift to purchasing instead of leasing by end-users and/or increased recycling or mine supply.

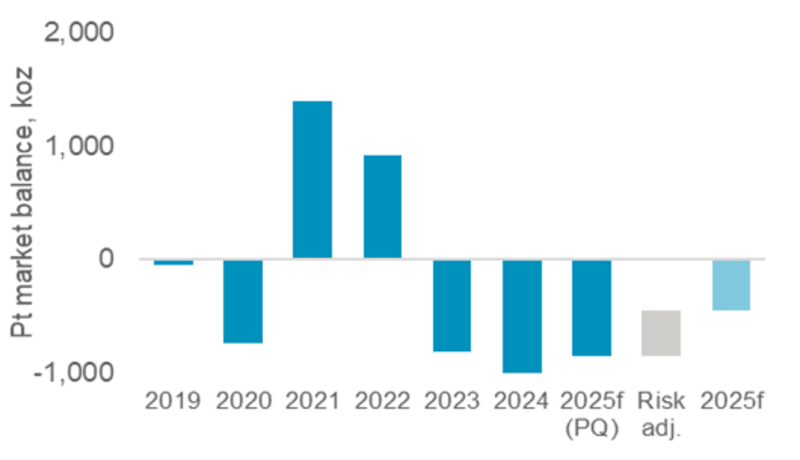

26 June 2025: Platinum supply and demand are price inelastic in the short-term, leading to sustained market imbalances: Platinum market deficits to persist as inelastic supply and demand are unlikely to react to rising prices: Despite the platinum price reaching a ten-year high, both supply and demand are expected to continue to show limited short-term price sensitivity. Costs, the economics of byproduct metals, and long lead times are constraints on mine supply. From a demand perspective platinum is essential in the majority of its end uses, especially in automotive and industrial applications, making them largely price inelastic in the near-term. As a result, the platinum market is still expected to post a near million-ounce deficit in 2025f.

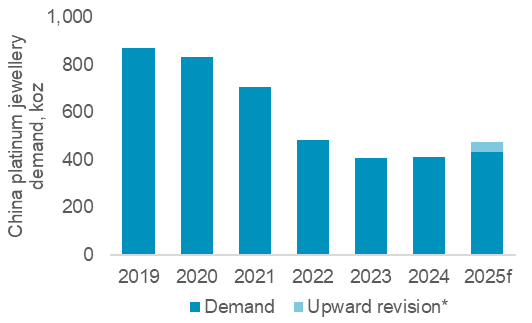

30 May 2025: Chinese platinum jewellery fabrication is growing rapidly as consumers turn away from expensive gold: Chinese platinum jewellery fabrication is growing rapidly as consumers turn away from expensive gold: In response to an exceptional rally in the gold price, which has weighed on demand and balance sheets, jewellery fabricators have shifted some inventory to lower priced platinum. With ten new platinum jewellery showrooms opening in Shuibei, China, so far in 2025, forecasts for China’s platinum jewellery fabrication demand have been revised upwards from 5% growth originally to 15% year-on-year growth to 474 koz in 2025f.

10 April 2025: Structural platinum market deficits will persist despite US tariffs and associated GDP risks: Structural platinum market deficits will persist despite US tariffs and associated GDP risks: The US’s imposition of wide-ranging tariffs on trading partners risks pushing the global economy into a recession or, at the very least, slowing GDP growth. Assessing the downside risks for platinum demand, we have used the supply chain disruptions of 2021/22 as a point of reference where platinum demand was its lowest in our time series. Positively, our conclusion is that structural demand changes, mitigate some downside scenario risks where platinum demand reductions are insufficient to eliminate the embedded deficit of 848 koz forecast for 2025.

28 March 2025: Platinum market deficit boosted by tariff-linked exchange stock movements that are unlikely to unwind anytime soon: Platinum market deficit boosted by tariff linked exchange stock movements that are unlikely to unwind anytime soon: The fear that tariffs will result in platinum being unavailable in the US at current prices has resulted in a steepening of the forward curve and significant inflows into NYMEX approved warehouses. Whilst trade tensions persist, we expect exchange stocks to remain elevated, but if tensions ease, only with material exchange stock outflows from current levels would the forecast 2025 deficit of 848 koz begin to reduce.

7 February 2025: Trump’s policies and the PGM markets Part 3: Rolling back environmental commitments and ‘Drill, baby, drill!’: Trump’s policies and the PGM markets Part 3: Rolling back environmental commitments and ‘Drill, baby, drill!’: Trump’s reductions of the US’s environmental commitments and “green” incentives, as well as his focus on increasing oil production, are expected to be net positive to PGM demand. Slower US BEV adoption increases PGM demand with each 1% reduction in BEV market share increasing 2E PGM demand by 25 koz per annum, which should more than offset any platinum demand lost from the US’s hydrogen plans.