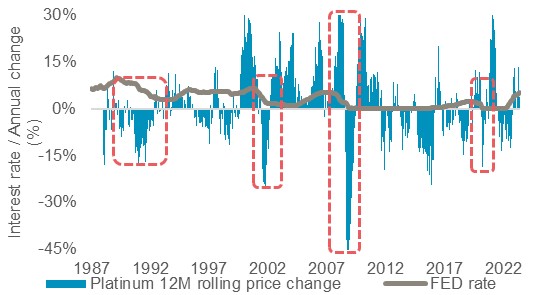

10 August 2023: Projected platinum supply/demand deficits should provide price support through economic downcycle: Analysis shows that the platinum price typically trends lower during economic down-cycles in combination with interest rate cuts. However, as the platinum market is forecast to enter a period of sustained deficits due to down-cycle resistant factors, we expect prices to prove more resilient during this cycle, or move higher.

Platinum Perspectives

WPIC® research is free of charge. It can be consumed by asset managers under MiFID II

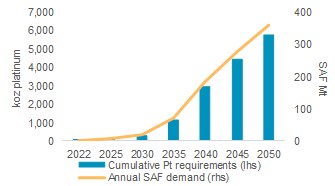

20 July 2023: Shanghai Platinum Week 2023: Key platinum demand takeaways and points of note: Shanghai Platinum Week 2023: Key platinum demand takeaways and points of note: WPIC co-hosted the third annual Shanghai Platinum Week (SPW) in the last week of June. This report highlights details of the conference as well as three key takeaways from the presentations that may influence future demand for platinum. The conference was attended by more than 650 delegates from over 400 organisations, with around 90 thousand watching online. Future SPW’s are scheduled for the second week of July (8-12 July 2024). There were too many topics discussed at the conference for us to cover them all. However, three topics; sustainable aviation fuel (SAF) automotive production forecasts for China, and projected fuel cell loadings stood out as having a bearing on future demand.

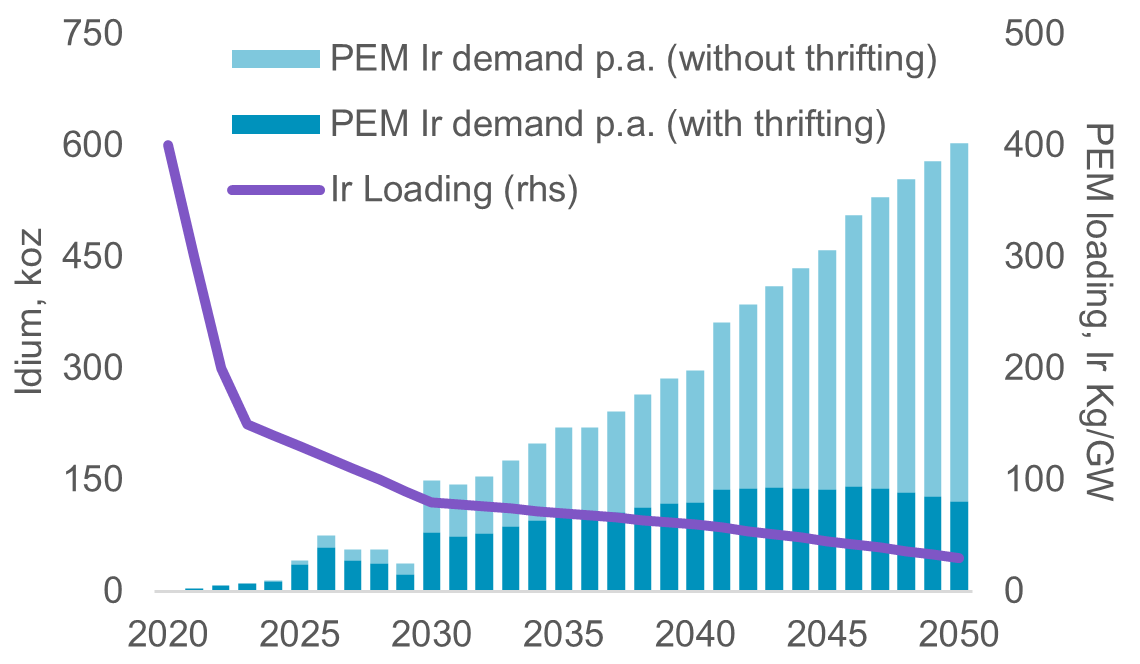

23 June 2023: Iridium availability is not a bottleneck to PEM electrolyser ramp-up; platinum demand from PEM electrolysers could reach >500 koz p.a. within 10 years: Allaying market fears, we do not expect iridium supply to impede the roll out of PEM electrolyser capacity. Electrolyser capacity is forecast to expand from <1GW to ~4,000 GW by 2050 (IEA). PEM technology is expected to achieve a >30% market share, facilitating the transition to green hydrogen. Despite the use of critical metals, thrifting, recycling and viable substitution in other applications will result in iridium supply being sufficient to meet identified demand and support cumulative installed PEM capacity of 1,550 GW by 2050.

1 June 2023: ETF investment returns: Growing investor appetite for platinum could deepen market deficit: South African investors have expanded their platinum ETF holdings by 430 koz year-to-date, as they see attractive upside for the metal in a market forecast to be in deficit by almost 1 Moz. In contrast, North American and European investors disposed of ETF holdings, reducing the net positive inflows to 300 koz versus only 30 koz included in the current outlook. As knowledge of the forecast record platinum deficit spreads, it is possible that ETF investor flows turn positive in North America and Europe, which could act to exacerbate the forecast deficit.

1 May 2023: How to solve an almost 1 Moz platinum market deficit: Our latest Platinum Quarterly highlighted a forecast record platinum market deficit of almost 1 Moz in 2023. Given the inelasticity of platinum supply, this shortfall has to be met from alternative sources such as above ground stocks. However, it is not known what platinum price will be necessary to attract the portion of above ground stocks required to meet the shortfall or indeed what impact having almost 80% of those above ground stocks locked-up in China will have on metal flows and price.

1 April 2023: China’s economic data gradually improved each month through Q1, resulting in Q1 2023 GDP growth of 4.5% exceeding consensus forecasts of 4.0%: China is the largest consumer of platinum globally. Following the easing of COVID restrictions, economic data suggests growing momentum in automotive output and retail jewellery. Should China’s economic data continue to improve through the course of the year, it could boost demand for platinum beyond current expectations. Should demand return to 2021 levels, that could imply an aggregate ~300 koz of incremental platinum demand relative to our latest Platinum Quarterly 2023 forecasts, further deepening the forecast 2023 deficit of 556 koz platinum.

1 March 2023: The significant existing market for grey hydrogen de-risks new green hydrogen projects supporting their growth and associated platinum demand: The installed production capacity for green hydrogen is doubling every two years, as are plans for new production capacity. Existing grey hydrogen demand exceeds 80 Mtpa, providing an existing mature end market for green hydrogen whilst fuel cell deployment grows. Furthermore, a mature grey hydrogen market suggests experience and technology for handling hydrogen already exists, even if the infrastructure is not yet widespread. We estimate that by the latter half of the 2030’s, hydrogen-related demand for platinum could equate to a third of all annual demand for platinum.

1 January 2023: Electricity shortages may elevate platinum’s historic January/February positive price seasonality in 2023: Over the past 25 years, the platinum price has shown the strongest positive price seasonality in January and February. The average compound return over those two months has been almost 8%. In contrast, platinum’s price performance has on average been more muted through the middle of the year. Calendar Q1, is also characterised by seasonally low refined mine supply from South Africa due to the challenges of restarting mining operations after the summer/Christmas holidays. This may be an influence on the typically strong January/February platinum price performance. With electricity supply shortages continuing in South Africa, it is possible that power shortages could add to the challenges associated with maintaining refined mine supply in the first quarter of 2023, which could exacerbate positive price seasonality.

1 December 2022: The nature and size of platinum above ground stocks now locked up in China combined with the 2023 forecast deficit could materially impact price discovery: China’s significant excess platinum imports since 2019 have resulted in a flow of metal out of Western vaults and into China and in 2020 and 2021 match or exceed the platinum market surpluses estimated for 2021 and forecast in 2022. The timing of China’s platinum purchases has been highly price opportunistic, which suggests that there is a quasi-speculative component to them. However, there has also been a step-change in total volumes since early 2021, indicating that there may also have been an increase in real demand. The concentration of above ground stocks in China leaves limited excess inventory in the rest of the world to meet any market imbalances, such as the 303 koz deficit forecast for 2023. This, in combination with higher prices likely being needed to release Chinese inventories to the domestic market, could have a significant bearing on platinum market price discovery.

1 November 2022: ETF disinvestment may reflect a change in investor preference to rather own physical platinum: In an ideal world with total asset class flexibility, investors would choose the lowest cost option for exposure to an underlying asset. Since mid-2021, the lowest cost option for platinum exposure has switched first from ETFs to futures, and then from futures to holding physical metal. Indeed, backwardation in the platinum forward curve means investors would effectively be being paid to hold a futures position in platinum, and for some investors the attraction to own and lease out physical platinum may have been even more compelling given significantly elevated platinum lease rates. This may be a factor in the significant disinvestment from platinum ETFs since the middle of 2021, which has totalled 850 koz.